Key Takeaways

-

India's CSR is entering Phase 3, moving beyond statutory compliance (Section 135 of the Companies Act, 2013) toward independently verified, outcome-driven impact aligned with SEBI's BRSR mandates and global ESG frameworks.

-

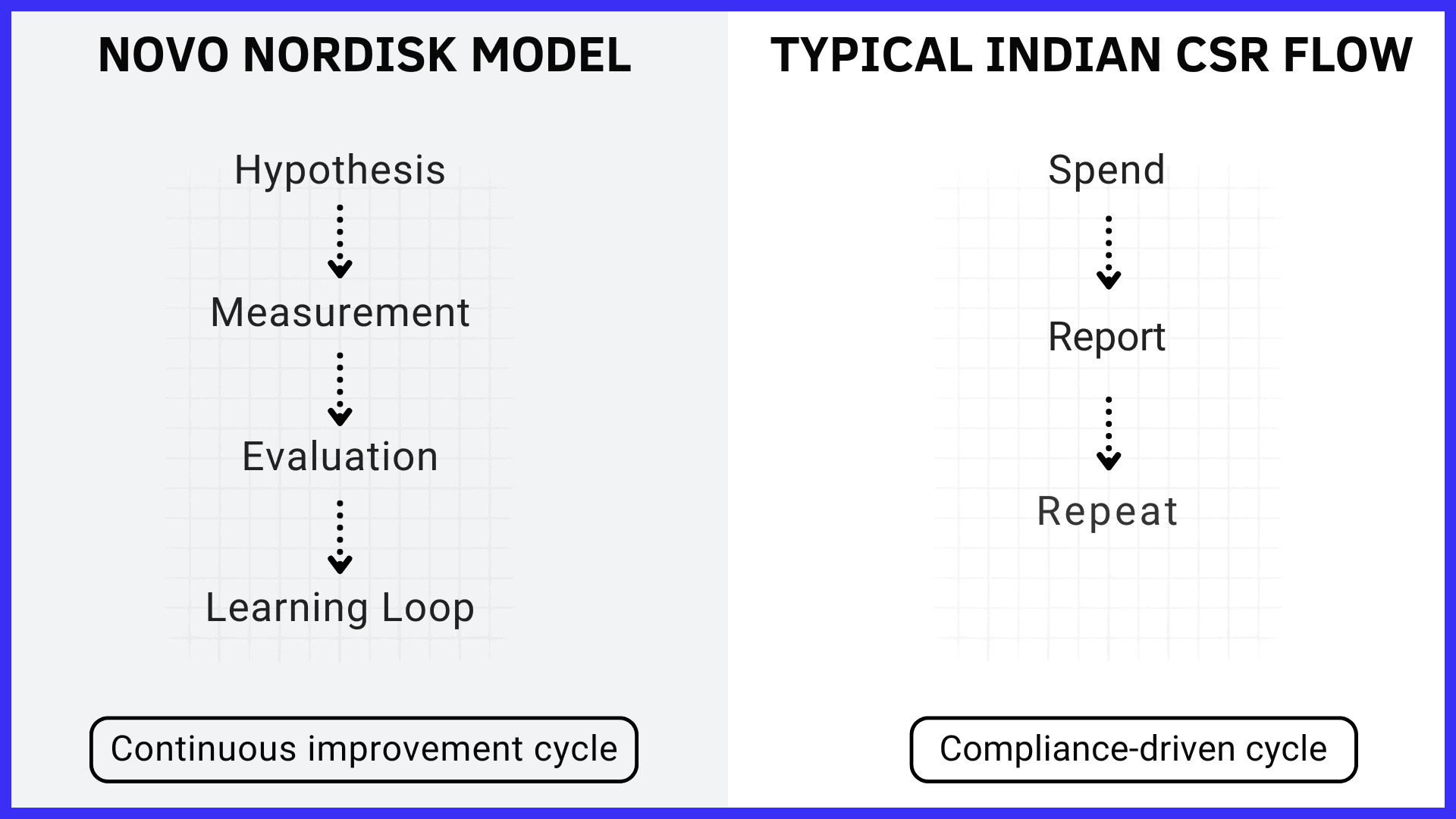

The defining failure of Indian CSR is not poor intent, but a structural measurement gap. Fewer than one in five large listed companies subject their CSR programs to independent third-party outcome assessment.

-

The companies generating the highest return on CSR investment, social and commercial, are those whose programs are a natural extension of what they actually know how to do well. Strategic alignment is not optional. It is the variable that separates impact from expenditure.

What Is Phase 3 of India's CSR Evolution?

In 2013, India did something no other nation had done: it made corporate social responsibility the law. Section 135 of the Companies Act mandated that eligible companies, those with a net worth of ₹500 crore or more, a turnover of ₹1,000 crore or more, or a net profit of ₹5 crore or more, direct 2% of their average net profits toward defined social causes.

The global business community watched with a mix of admiration and scepticism. More than a decade later, the law has done what it was designed to do. It forced companies to show up. Annual CSR spending now runs into tens of thousands of crores. Foundations have been established, programs launched, and annual reports filled with impact narratives.

But showing up is not the same as mattering.

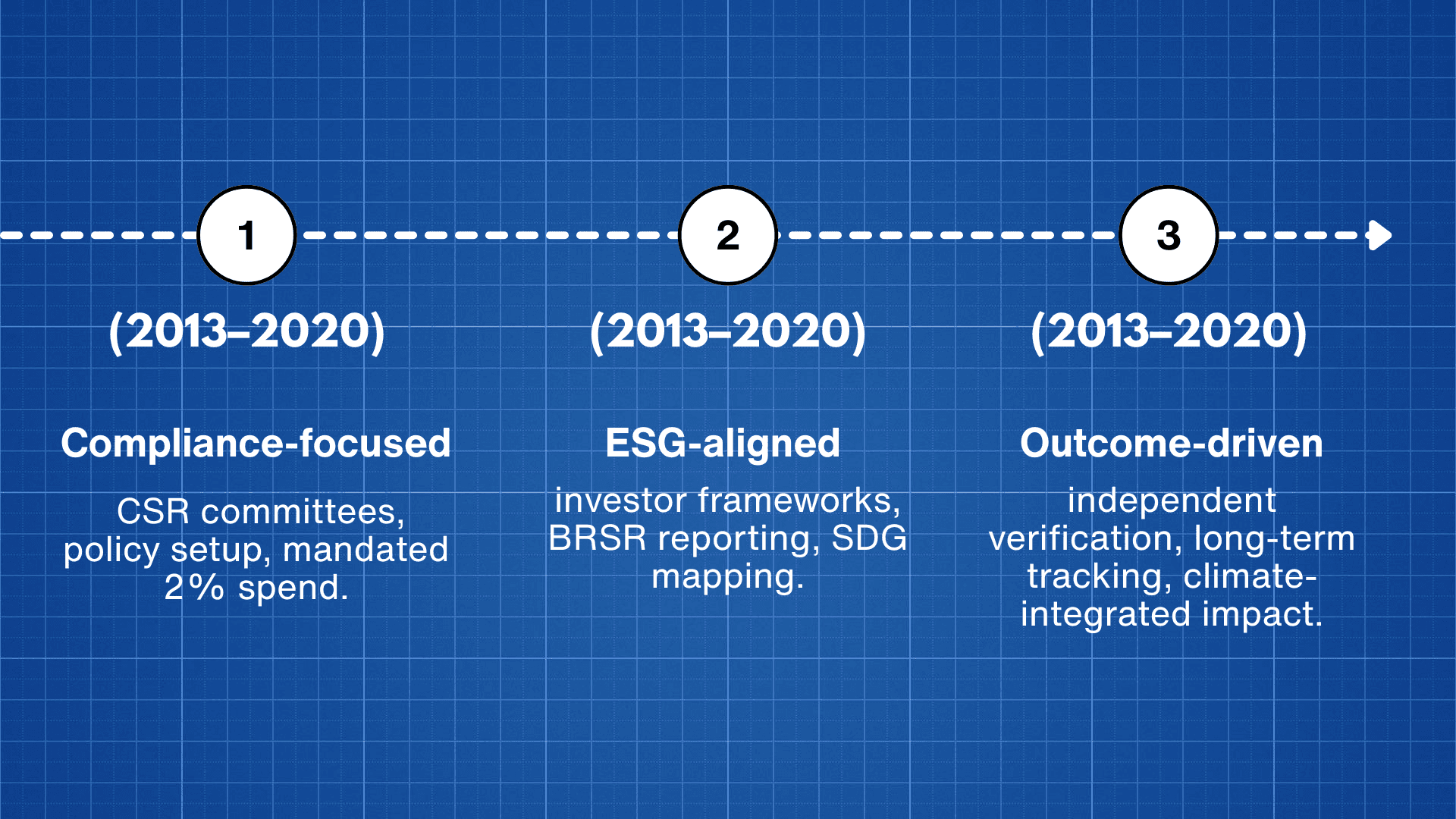

India's CSR landscape has moved through two distinct phases, and is now entering a third:

Phase 1 (2013–2020): Institutional compliance, forming CSR committees, setting policies, and spending the mandated 2%. Phase 2 (2021–2024): ESG alignment connecting programs to investor frameworks, BRSR disclosures, and SDG mapping. Phase 3 (2025–onward): Outcome accountability independently verified, longitudinally tracked, climate-integrated impact.

The question is no longer whether Indian companies invest in society. It is whether that investment generates verifiable, lasting change or sophisticated-looking inertia.

3 Reasons CSR Accountability and ESG Scrutiny Are Increasing

Three forces are converging to transform CSR from a statutory line item into a strategic liability or advantage.

1. Investor scrutiny now has direct financial consequences. Global institutional investors no longer treat ESG disclosures as supplementary reading. They embed environmental exposure, governance quality, and social impact credibility directly into valuation models. A CSR program that cannot demonstrate measurable outcomes is not uninspiring; it is a signal of weak risk management. For companies seeking international capital or inclusion in ESG indices, this distinction carries a cost of capital implication.

2. Regulatory frameworks have structurally hardened. SEBI's BRSR mandate has moved sustainability disclosures from voluntary narrative to structured accountability. Unspent CSR funds now face stricter protocols under amended Companies Act rules. The era of the soft audit is ending. Companies that treat disclosure as a communications exercise rather than a governance obligation are increasingly exposed to regulatory risk.

3. Verification technology has outpaced self-reporting. Satellite imagery, AI-assisted data analysis, longitudinal health datasets, and third-party audit firms have made it substantially harder to sustain a gap between stated impact and actual outcomes. Companies that built reputations on "scale reached" are finding that external data tells more honest stories than annual reports do.

What Is the Accountability Gap in Indian CSR?

The accountability gap is the measurable distance between what Indian CSR reports claim to have achieved and what can be independently verified as having actually changed.

It is not a fringe problem. It is the defining structural weakness of the entire CSR ecosystem, and it is wider than most boards realise.

Output vs. Outcome: The Core Distinction

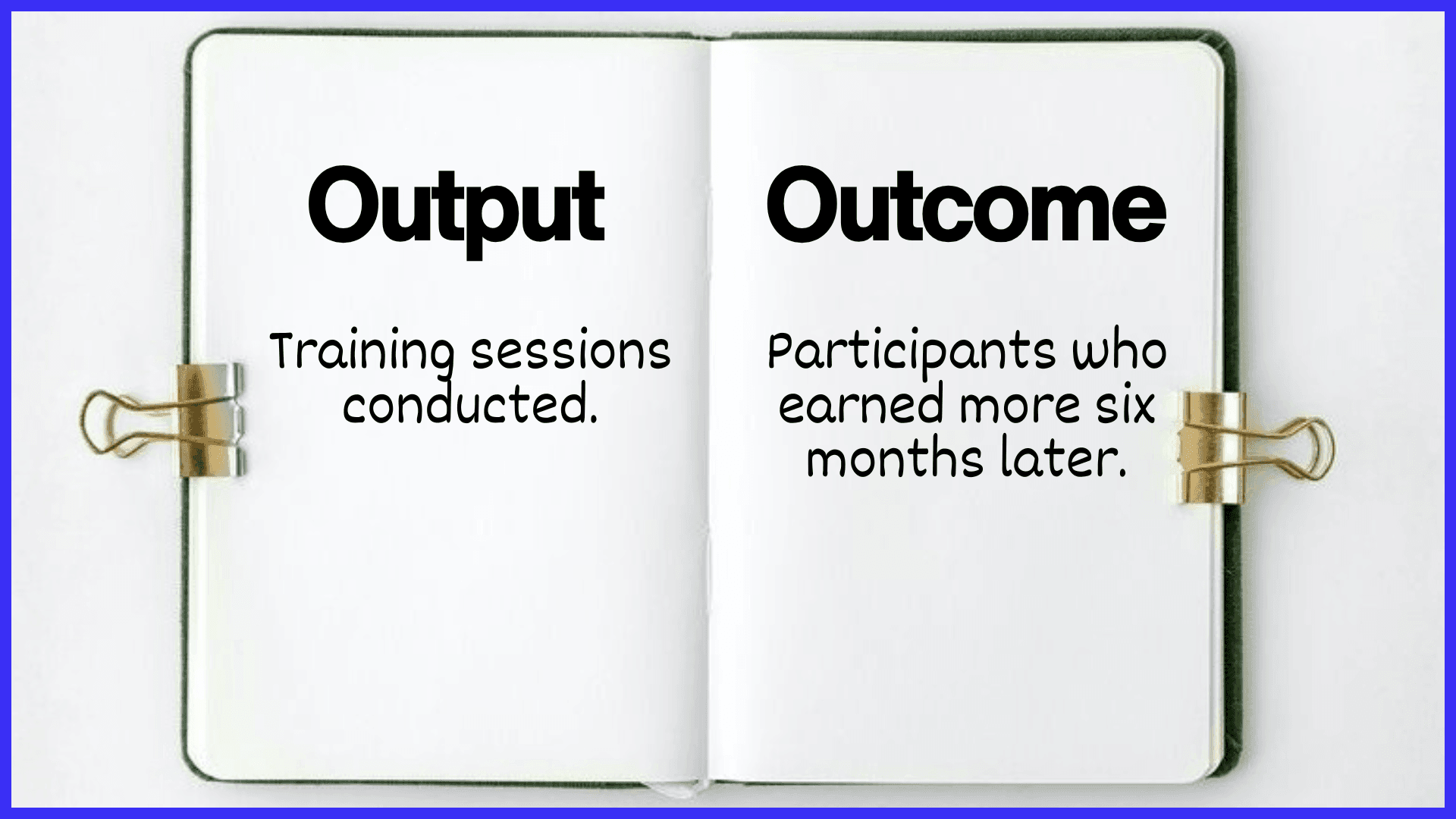

Most Indian CSR reporting measures outputs activity completion metrics such as beneficiaries reached, infrastructure units built, and training sessions conducted. These are inputs to social change, not evidence of it. The critical leap from "we ran this program" to "this program produced this measurable, durable improvement in people's lives" is where Indian CSR systematically fails.

Self-Concealing Failure: Why the Gap Is Hard to See

The accountability gap has a compounding characteristic: it is self-concealing. When impact is measured only by the program designer, using internally defined metrics, filtered through a communications-reviewed annual report, the system has no natural mechanism for surfacing failure. Unsuccessful programs look identical to successful ones on paper. This is not dishonesty; it is the predictable outcome of a measurement architecture designed for optics rather than organisational learning.

SROI: Cited, Rarely Calculated

Social Return on Investment remains more a boardroom phrase than a functioning discipline. Fewer than one in five large listed Indian companies commission independent third-party outcome assessments. Most CSR reports are written to satisfy regulatory disclosure requirements, not to answer the harder question of whether anything durably changed.

The Infrastructure Gap

The failure is structural. Companies have invested heavily in CSR program delivery and almost nothing in CSR measurement infrastructure. The result is a landscape where tens of thousands of crores move annually with limited accountability for what they produce. What the third phase demands is a fundamentally different architecture: independent evaluators, longitudinal tracking systems, and public reporting standards that separate what was claimed from what was confirmed.

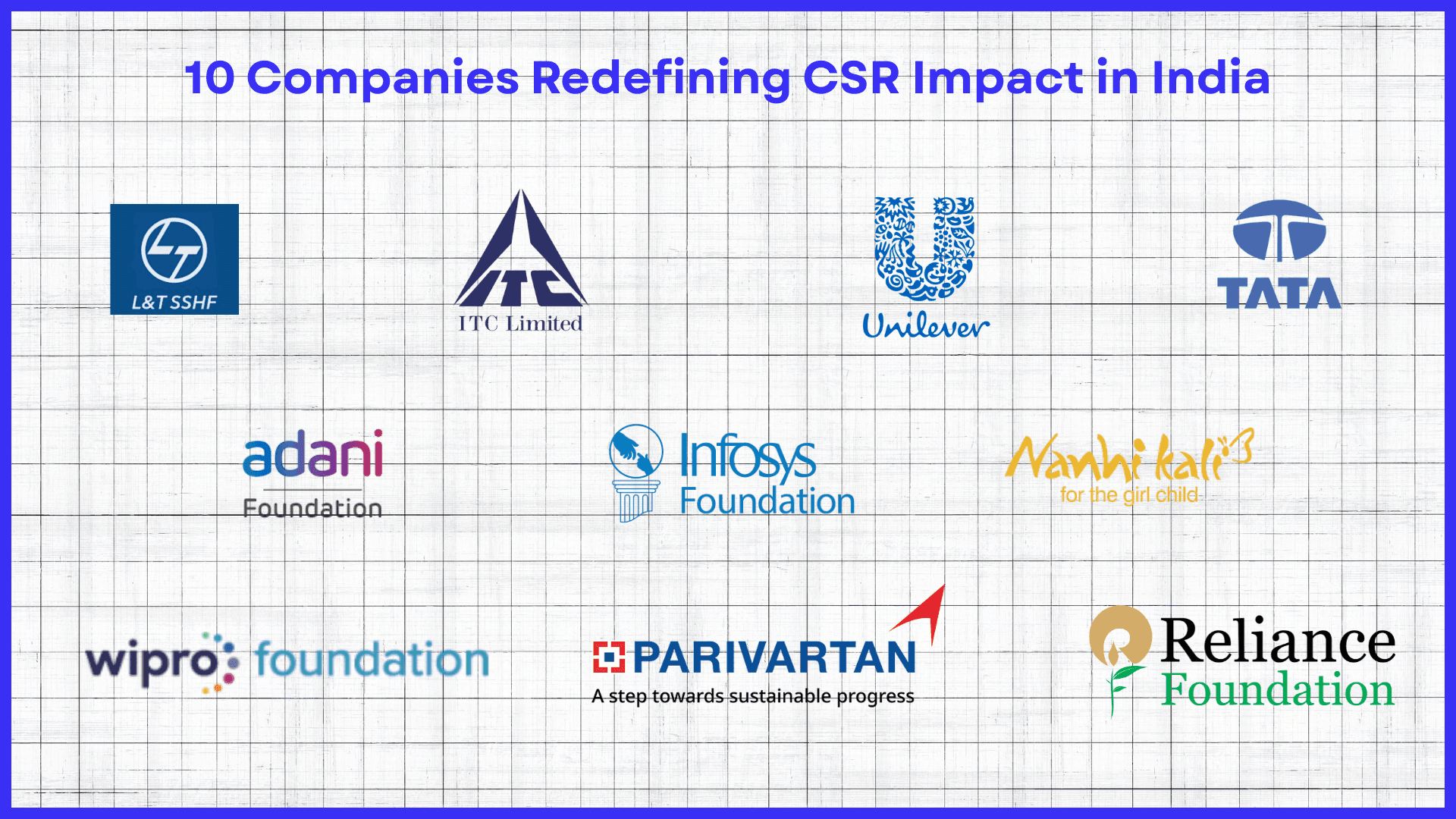

10 Companies Redefining CSR Impact in India: A Comparative Overview

The following cases are not simply success stories. They are evidence of a structural argument: CSR generates its highest return social and commercial, when it is a natural extension of what a company actually knows how to do well.

| Company | Primary CSR Focus | Core Strength | The Accountability Challenge |

|---|---|---|---|

| Tata Group | Multi-sector: health, education, rural uplift | Structurally embedded philanthropy via Tata Trusts | Compelling narratives without SROI-validated outcomes |

| Reliance Foundation | Rural transformation, healthcare, disaster response | Corporate infrastructure mobilised at the national scale | Scale metrics masking uneven, unverified local impact |

| Infosys Foundation | Digital inclusion, education infrastructure | Benchmark governance, BRSR compliance, third-party audits | Access metrics without learning outcome evidence |

| Mahindra (Nanhi Kali) | Girl child education | Sustained, focused single-issue commitment | No lifecycle tracking of girls post-education |

| ITC Limited | Environmental sustainability, regenerative agriculture | Carbon, water, and waste-positive for two decades | Self-declared green credentials without forensic verification |

| HDFC Bank (Parivartan) | Financial inclusion, rural literacy | Banking expertise deployed as social infrastructure | Analogue literacy tools in a digital-native financial world |

| Wipro Foundation | Education system reform, ecological restoration | Systems-level thinking over surface interventions | Depth of impact invisible in standard ESG reporting formats |

| Hindustan Unilever | Hygiene and sanitation behaviour change | Category expertise: product knowledge + distribution reach | Thin boundary between social impact and brand promotion |

| L&T (Skill Forge) | Vocational training for infrastructure trades | Direct alignment with verified national workforce gap | Traditional skill credentials in a BIM and AI-driven industry |

| Adani Foundation | Rural infrastructure near operational sites | Place-based precision, community trust at scale | Proximity-led programs without independent impact verification |

1. Tata Group: When Philosophy Must Meet Proof

Tata's CSR model is unlike any other in India, because it is not really a "model" at all. With Tata Trusts holding around two-thirds of the equity in Tata Sons, social purpose is architecturally embedded in the ownership structure itself. The Tata Memorial Centre, the Tribal Development Society under Tata Steel, and skilling programs under Tata Motors are not additions to the business. They are part of its original design.

The challenge, as India's third CSR phase demands, is that even the most credible legacy must now be audited. Compelling stories of rural upliftment in Jharkhand or cancer care expansion in Mumbai carry diminishing persuasive weight when institutional investors want Social Return on Investment ratios, longitudinal outcomes, and externally verified impact. Tata's next chapter is not about doing more; it is about proving more, with the same precision it brings to engineering.

2. Reliance Foundation The Scale Trap

During the COVID-19 crisis, Reliance Foundation demonstrated something remarkable: that corporate infrastructure logistics networks, digital platforms, and manufacturing capacity could be mobilised as national relief infrastructure faster than many government departments.

Reliance reached tens of millions. They were on the ground building hospitals, moving PPE, and getting oxygen plants online when the country needed it most. Looking back, that level of mobilisation was nothing short of remarkable.

But scale has a shadow. "Millions reached" is an input metric masquerading as an outcome metric. It describes reach, not transformation. The critical question is, What percentage of rural communities saw sustained income improvement? What is the five-year health trajectory of beneficiaries? remain underanswered in Reliance's public reporting.

The Foundation has cracked mobilisation. The harder problem is measurement. Moving from logistics-grade efficiency to evidence-grade accountability is the next frontier.

3. Infosys Foundation Governance as a Ceiling

Infosys Foundation is arguably the most rigorously governed CSR institution in India. Its BRSR compliance, third-party audits, and structured disclosures set a benchmark that most companies have not yet reached.

But in 2026, governance quality alone is not sufficient. The harder test is whether governance produces outcomes, not just clean processes. The distinction between "schools digitised" and "students whose learning trajectories improved" is not administrative; it is existential to the program's credibility.

Infosys has a structural advantage here that it has not yet fully deployed: it is one of the world's leading technology companies. The same AI and data engineering capabilities that serve its global clients could build adaptive learning platforms, predict dropout risks, and measure cognitive uplift at scale. This is not a theoretical possibility; it is a strategic obligation.

4. Mahindra's Nanhi Kali: The Power and Limit of Focus

Among India's ten largest CSR spenders, Mahindra has made perhaps the most intellectually coherent choice: concentrate resources on one problem, over a long period, with structured tracking. Nanhi Kali's focus on girl child education, aligned explicitly with SDG 4 and SDG 5, avoids the dilution that scatters impact across too many sectors.

The program tracks attendance, academic performance, and retention. That discipline is genuinely rare. But the next accountability standard asks a harder question: what happened after? Not "how many girls completed school," but "how many moved into economic independence, professional careers, leadership roles?"

Lifecycle data, the longitudinal tracking of beneficiaries into adulthood, is the frontier Nanhi Kali must now cross. Focus is a strength. Incomplete timelines weaken the argument.

5. ITC Integration as Strategy, Verification as the Next Step

ITC's sustainability record is genuinely remarkable. Carbon-positive since 2006. Water-positive since 2002. Solid waste recycling-positive since 2005. These are not marketing claims; they reflect decades of deliberate supply chain integration, regenerative agriculture programs, and watershed management.

More than any other company on this list, ITC has demonstrated that environmental sustainability and business performance are not in tension. Its model is a direct rebuttal to the argument that ESG costs a margin.

The challenge now is not doing more, it is proving what has been done. Scope 3 emissions accounting, TCFD-aligned climate risk disclosures, and externally audited biodiversity metrics have become the standard against which legacy sustainability claims are now measured. Satellite data and AI-driven emissions tracking tools mean that corporate self-declarations are increasingly verifiable or falsifiable. ITC's credibility is strong enough to welcome that scrutiny. The question is whether its reporting architecture is ready for it.

6. HDFC Bank's Parivartan: The Digital Inclusion Gap

HDFC Bank's Parivartan initiative is an elegant example of CSR aligned with core competence. As India's largest private lender, HDFC has structured its social programs around financial literacy, self-help group empowerment, micro-entrepreneur credit access, and rural banking infrastructure. The result is a CSR that simultaneously serves communities and develops future customers through a coherent strategic loop.

The blind spot is temporal. Parivartan's financial literacy programs were designed for a world where banking access was the primary barrier. In a country where UPI processes billions of monthly transactions and fintech platforms are redefining financial behaviour, the more urgent literacy challenge is digital: understanding AI-driven credit scoring, recognising fraud, and navigating data privacy.

The program's analogue heritage is a strength in depth and trust. Its next evolution is digital fluency teaching, not just how to bank, but how to operate safely and confidently in a financial system increasingly governed by algorithms.

7. Wipro Foundation: The Invisible Work Problem

Wipro Foundation operates from a conviction that most CSR programs share but few execute: the highest-leverage interventions happen at the level of systems, not symptoms. Rather than building schools, Wipro invests in teacher quality. Rather than funding NGO projects, it builds NGO institutional capacity. Rather than planting trees, it restores ecological systems.

This is intellectually correct. It is also strategically vulnerable. Systems-level work resists easy measurement. It is hard to summarise in an annual report, harder still to compare against a competitor who built fifty classrooms.

Wipro's challenge is not doing the work but making the work visible in a metrics-driven ESG environment. AI-powered dashboards that connect teacher capacity interventions to student learning outcomes, or blockchain-verified NGO performance tracking, would not compromise the depth of Wipro's approach. They would give it the visibility it deserves.

8. Hindustan Unilever Expertise as Legitimacy

HUL's hygiene and sanitation programs represent the most strategically coherent model on this list in one specific sense: the company is genuinely expert in the domain it is investing in. When HUL runs handwashing campaigns, it brings product formulation knowledge, behavioural science expertise, and distribution infrastructure that no external CSR agency can replicate.

The credibility risk is the proximity between brand promotion and social impact. This is not a cynical observation; it is a structural challenge that comes with category-aligned CSR. The way through is clinical evidence. Randomised controlled trials measuring disease incidence before and after program deployment, linked to national health data systems, would transform HUL's impact claims from plausible to proven. That kind of evidence would also be genuinely useful to public health policy, which is the clearest signal that a CSR program has transcended promotion.

9. L&T Skill Forge Right Strategy, Accelerating Obsolescence

L&T's vocational training programs for construction trades are arguably the most directly aligned CSR initiative in India to a verified national need. India's infrastructure expansion, including highways, ports, smart cities, and renewable energy installations, requires trained tradespeople faster than the formal education system can produce them. L&T trains welders, electricians, masons, and project supervisors, then places them into an industry it knows intimately.

The model is sound. The risk is the speed of change. AI-assisted design, Building Information Modelling, green construction standards, and net-zero building codes are reshaping what infrastructure work requires. A training program that produces skilled tradespeople without digital literacy or sustainability certification credentials will find its graduates increasingly underqualified for the projects they are meant to build.

L&T's advantage is that it knows exactly where the industry is going. Embedding that intelligence into curriculum design, VR construction simulators, green building certification tracks, and BIM literacy would keep the program ahead of disruption rather than behind it.

10. Adani Foundation Proximity Is Powerful, Opacity Is Dangerous

Adani Foundation's place-based approach, concentrating programs in communities adjacent to ports, power plants, and infrastructure corridors, is strategically coherent. It addresses the most immediate and legitimate concern that large-scale industrial development creates: displacement and marginalisation of local populations. By converting potential conflict zones into partnership zones, the Foundation earns the social license that long-term project viability requires.

The challenge is that in 2026's ESG environment, proximity-based impact is held to the highest evidentiary standard precisely because the incentive to conflate compliance-mandated rehabilitation with voluntary social investment is real. Global investors equipped with satellite-based environmental monitoring and AI-driven compliance audit tools require clear delineation. Independent verification, blockchain-tracked community outcomes, and TCFD-aligned climate disclosures would transform the Foundation's credibility from locally earned to globally defensible.

What Good Actually Looks Like: A Global Reference Point

What Distinguishes Excellence from Compliance

Across these ten cases, three patterns separate high-performing CSR from its well-funded but underperforming counterpart.

Strategic alignment multiplies impact. ITC, HDFC, and L&T all demonstrate that when CSR leverages genuine corporate expertise in agriculture, financial systems, and infrastructure, respectively, the resulting programs are more credible, more durable, and more efficient than externally commissioned philanthropy. The company knows the domain. The community benefits from that knowledge.

Focus outperforms dispersion. Mahindra's decision to concentrate on a single social challenge over a sustained period produces cleaner outcomes and sharper accountability than programs spreading resources across six or seven thematic areas to satisfy a Schedule VII checklist. Concentrated investment is harder to report as "comprehensive," but it is easier to evaluate as meaningful.

Longitudinal commitment changes the nature of what is possible. The most credible programs in this analysis, Tata's healthcare institutions, Wipro's education system work, and Mahindra's Nanhi Kali share a decade or more of continuous investment. This is not sentimentality. Multi-year programs can track beneficiary trajectories, iterate on what works, and build community trust that one-off projects cannot approximate.

The Board's Role: Accountability Starts at the Top

Every CSR shortcoming documented in this article, the measurement gap, the scale trap, and the transparency deficit, is ultimately a governance failure. And governance, in a corporate context, lives or dies at the board level.

India's Companies Act requires eligible companies to form a CSR committee of the board. In practice, this requirement has largely produced compliance theatre: a committee that meets quarterly, reviews expenditure reports, and approves budgets. What it rarely produces is genuine strategic oversight, the kind where a director asks not "Did we spend the 2%?" but "What did we learn from last year's programs that changed how we designed this year's?"

Boards set the cultural permission for accountability. When a board treats CSR as a regulatory checkbox, the executive team receives an unambiguous signal: delivery matters, measurement does not. When a board treats CSR outcomes with the same seriousness it brings to financial performance, demanding independent verification, longitudinal tracking, and honest failure analysis, the entire program architecture shifts.

Three questions should be non-negotiable at every CSR committee meeting, and currently are not asked at most of them:

-

What did our programs not achieve that we expected them to? The absence of honest failure analysis from virtually every Indian CSR report is not evidence of uniformly successful programs. It is evidence of a governance culture that has not created space for honesty.

-

Who outside our organisation has verified our impact claims? Third-party assessment is not expensive relative to CSR budgets. Its absence is a choice, not a constraint.

-

What is the five-year trajectory of a beneficiary who entered our flagship program three years ago? If a board cannot answer this, the program has no longitudinal tracking, and every impact claim is a snapshot presented as a story.

CSR in India will not mature through regulation alone. Regulators can mandate spending, disclosure, and committee formation. They cannot mandate the quality of questions asked in a boardroom. That is a leadership choice, and it is the choice that separates organisations whose CSR genuinely matters from those whose CSR merely complies.

Six Questions Every CSR Committee Should Be Asking Right Now

Thought leadership without practical application is commentary. The following questions are diagnostic, designed not for annual reports, but for the honest internal conversations that precede them. A CSR committee that can answer all six with evidence is ahead of ninety per cent of its peers. One that struggles to answer more than two has identified its most important strategic priority.

One: Can you trace a single beneficiary's outcome five years after they exited your flagship program? Not an anecdote selected for the annual report. A systematically tracked data point from a representative sample. If the answer is no, the program has no longitudinal architecture and every impact claim it makes is, at best, a well-intentioned estimate.

Two: Who outside your organisation calculated your impact numbers? If the answer is your internal team, your communications agency, or your implementation partner, the numbers are not independently verified. That is not a moral failing; it is a credibility gap that sophisticated investors and regulators are increasingly equipped to identify.

Three: What did your CSR programs fail to achieve last year, and what did you change as a result? The absence of an answer to this question is one of the most reliable indicators of a compliance-oriented CSR culture. Programs that are never documented as failing are programs that are never honestly evaluated.

Four: Is your CSR strategy designed around what your company knows how to do well, or around what looks good in a Schedule VII checklist? The difference between category-aligned CSR, where corporate expertise amplifies social impact and checklist CSR is not always visible from the outside. It is almost always visible in program outcomes.

Five: If your CSR budget were cut by thirty per cent tomorrow, which programs would you protect and why? The answer reveals which programs are genuinely strategic and which exist to fill a spending requirement. The ones worth protecting are the ones with evidence of impact, institutional relationships, and a coherent theory of change. The others are worth reconsidering even without the hypothetical budget pressure.

Six: Are your ESG disclosures and your CSR reports telling the same story? As BRSR requirements tighten and CSR feeds directly into sustainability reporting architecture, inconsistencies between these two documents are increasingly visible to analysts and auditors. Alignment is not just an administrative convenience; it is a governance signal.

These questions are not comfortable. They are not designed to be. The CSR committees that ask them honestly, document the answers, and act on the gaps are the ones building programs that will hold up to the scrutiny of India's third CSR phase. The ones that avoid them are building reputational exposure that they have not yet priced.

CSR Accountability Checklist for Board Committees

Use this checklist to assess your organisation's CSR accountability posture before your next board review.

Longitudinal tracking: Can we trace a single beneficiary's outcome five years after they exited our flagship program, using systematic data, not a selected anecdote? Independent verification: Were our impact numbers calculated by someone outside the organisation, not our internal team, communications agency, or implementation partner? Failure documentation: Can we name what our CSR programs failed to achieve last year, and identify what we changed as a result? Strategic alignment: Is our CSR strategy built around what our company genuinely knows how to do well or around what satisfies a Schedule VII checklist? Priority clarity: If our CSR budget were cut by 30% tomorrow, do we know which programs we would protect and why based on impact evidence? Reporting consistency: Are our ESG disclosures and our CSR reports telling the same story, with no material inconsistencies visible to an external analyst?

A board that can answer all six with evidence is ahead of the large majority of Indian listed companies. One that struggles with more than two has found its highest-priority strategic gap

Conclusion: What the Next Phase of Indian CSR Actually Requires

India's CSR mandate forced companies to invest in society. Phase 3 will require them to prove it worked.

The ten companies in this article are not failing; many of them are doing genuinely important work. But in a landscape where BRSR reporting is mandatory, ESG scrutiny is intensifying, and AI-assisted verification tools are closing the gap between stated and actual impact, the era of narrative-led CSR is ending.

What replaces it is not more spending. It is a better measurement. Independent verification. Longitudinal outcome tracking. Governance that treats social impact with the same discipline as financial performance.

The companies that adapt early will hold a meaningful advantage in ESG positioning, investor trust, regulatory goodwill, and community legitimacy. The ones that wait will find that compliance, once the floor, has become the ceiling.

India pioneered mandatory CSR. The next benchmark is measurable CSR. That transition is already underway, and the companies that lead it will define what responsible business looks like for the next generation.

Frequently Asked Questions

How does BRSR impact CSR spending in India?

BRSR (Business Responsibility and Sustainability Reporting) mandates that CSR outcomes feed into a standardised data format. This prevents "standalone narratives" and forces companies to provide comparable, quantitative data that investors can benchmark.

What is the penalty for unspent CSR funds?

Under Section 135, unspent funds must be transferred to government-designated accounts or a separate "Unspent CSR Account" for ongoing projects. Failure to comply leads to significant financial penalties for the company and its officers.

How can Indian companies measure Social Return on Investment (SROI)?

SROI measurement requires four components: defined outcome indicators, a counterfactual baseline, monetisation of non-financial benefits, and independent verification. Companies should start by piloting SROI for one flagship program rather than attempting it for all projects at once.

Why is third-party verification important for CSR in India?

Third-party verification is important for three distinct reasons. First, credibility: independently verified impact claims are substantially more persuasive to institutional investors, ESG rating agencies, and regulators than self-reported numbers. Second, organisational learning: external evaluators surface program failures that internal reporting systems are structurally incentivised to conceal. Third, regulatory alignment: as BRSR requirements tighten and SEBI's oversight increases, the gap between self-reported and independently verified data is becoming a material disclosure risk.

What is the difference between CSR output and CSR outcome?

An output is what a program does: the number of training sessions conducted, schools built, or beneficiaries enrolled. An outcome is what changes as a result of whether participants earn more, learn more, or live healthier lives. Indian CSR reporting is dominated by output metrics because they are easier and cheaper to count. Outcome measurement requires longitudinal tracking, control groups, and independent evaluation. The shift from output to outcome reporting is the central accountability challenge of India's Phase 3 CSR evolution.

Which Indian companies have the most credible CSR programs?

Credibility in CSR depends on three factors: strategic alignment with core business expertise, longitudinal commitment over multiple years, and transparent impact reporting with independent verification. By these criteria, Infosys Foundation leads on governance transparency and disclosure quality; ITC leads on business-integrated sustainability with a multi-decade track record; and Mahindra's Nanhi Kali leads on focused, structured social intervention with tracked program metrics. All, however, face the same Phase 3 challenge: translating program delivery into independently verified outcome evidence.