What Is BRSR? SEBI's Mandatory ESG Disclosure Framework for India's Top 1,000 Listed Companies

Business Responsibility and Sustainability Reporting is a mandatory disclosure mechanism notified by SEBI that requires the top 1,000 listed companies in India to report their performance against Environmental, Social, and Governance (ESG) parameters. Unlike previous formats, BRSR is designed to be quantitative and verifiable.

What is BRSR Core?

BRSR Core constitutes a compulsory subset of the broader Business Responsibility and Sustainability Report (BRSR). Introduced by SEBI in 2023, it consists of 9 critical ESG attributes (such as GHG emissions, water usage, and gender pay gap) that require Reasonable Assurance, a high-level third-party audit to ensure data is accurate, verifiable, and free from greenwashing.

What SEBI Is Actually Building: The 3 Strategic Goals Behind BRSR Core

SEBI didn't design BRSR Core to generate more paperwork. It was designed to address a specific, long-standing issue in Indian capital markets: the complete lack of ESG data that investors could actually rely on. Three strategic objectives sit at the heart of that design, and understanding them changes how you approach compliance:

-

Radical Standardisation: Because inconsistent data is the same as no data. For years, "carbon intensity" was whatever a company's sustainability team decided it meant. Different boundaries, different denominators, different assumptions, all buried inside reports that looked authoritative but couldn't be compared. BRSR Core replaces that ambiguity with a single, mandatory definition applied uniformly across every sector. A steel plant in Odisha and a fintech firm in Bengaluru now speak the same measurement language. That consistency is not administrative tidiness. It is the foundation on which investor trust is built.

-

Evidence over assertion: The end of sustainability as storytelling. The most consequential shift in BRSR Core isn't what it measures; it's the standard to which those measurements must be held. Nine KPIs covering emissions, water, energy, waste, safety, gender pay, sourcing, inclusive employment, and customer protection must now be traceable to source documents and verified by an independent auditor. "We care about the environment" was once a disclosure. Under Reasonable Assurance, it is an opening argument that must survive cross-examination.

-

Global legibility: Because Indian capital markets compete internationally. Domestic ESG reporting that only makes sense to domestic readers has a ceiling. SEBI recognised this early. By aligning BRSR Core with ISSB and GRI frameworks and mandating PPP-adjusted intensity ratios that strip out currency and cost-of-living distortions, SEBI has done something structurally significant: it has made Indian ESG data readable, comparable, and trustworthy to a fund manager in London, Singapore, or New York. That is not a reporting feature. It is a market access strategy, and it is the reason a fund manager in Singapore can now run a screener on Indian mid-caps and get data she trusts."

The Difference Between BRSR and BRSR Core

While often used interchangeably, BRSR and BRSR Core serve different regulatory functions.

- Think of BRSR as your company's "Annual ESG Report Card".

- Think of BRSR Core as the "Audited Final Exam".

While the full BRSR allows for narrative explanations regarding CSR initiatives, BRSR Core is a specific subset of data points that must undergo Reasonable Assurance.

| Feature | Full BRSR | BRSR Core |

|---|---|---|

| Scope | Comprehensive: Covers 9 Principles of NGRBC. | Focused Subset: Covers 9 specific ESG Attributes. |

| Indicators | 140+ Indicators (Essential & Leadership). | Select Key Performance Indicators (KPIs). |

| Verification | Self-certified by the company. | Requires Reasonable Assurance (Audit). |

| Intensity Ratios | Based on raw revenue figures. | Adjusted for Purchasing Power Parity (PPP). |

| Primary Goal | Broad transparency and stakeholder communication. | High-fidelity data for global investor comparability. |

| Applicability | Mandatory for the top 1,000 listed entities. | Phased rollout for top 1,000 entities (Audit focus). |

Key Distinctions to Remember:

-

Assurance Level: The full BRSR does not legally require a third-party audit of all its narrative sections. However, the BRSR Core must be audited by an independent assurance provider to provide "Reasonable Assurance."

-

Global Alignment: BRSR Core introduces PPP-adjusted intensity ratios, making it easier for international investors to compare an Indian company’s carbon or water footprint with global peers on a level playing field.

-

The "Auditor" Factor: Because BRSR Core requires a signature from an external auditor, the data governance required for Core is much stricter than the general disclosures in the full BRSR.

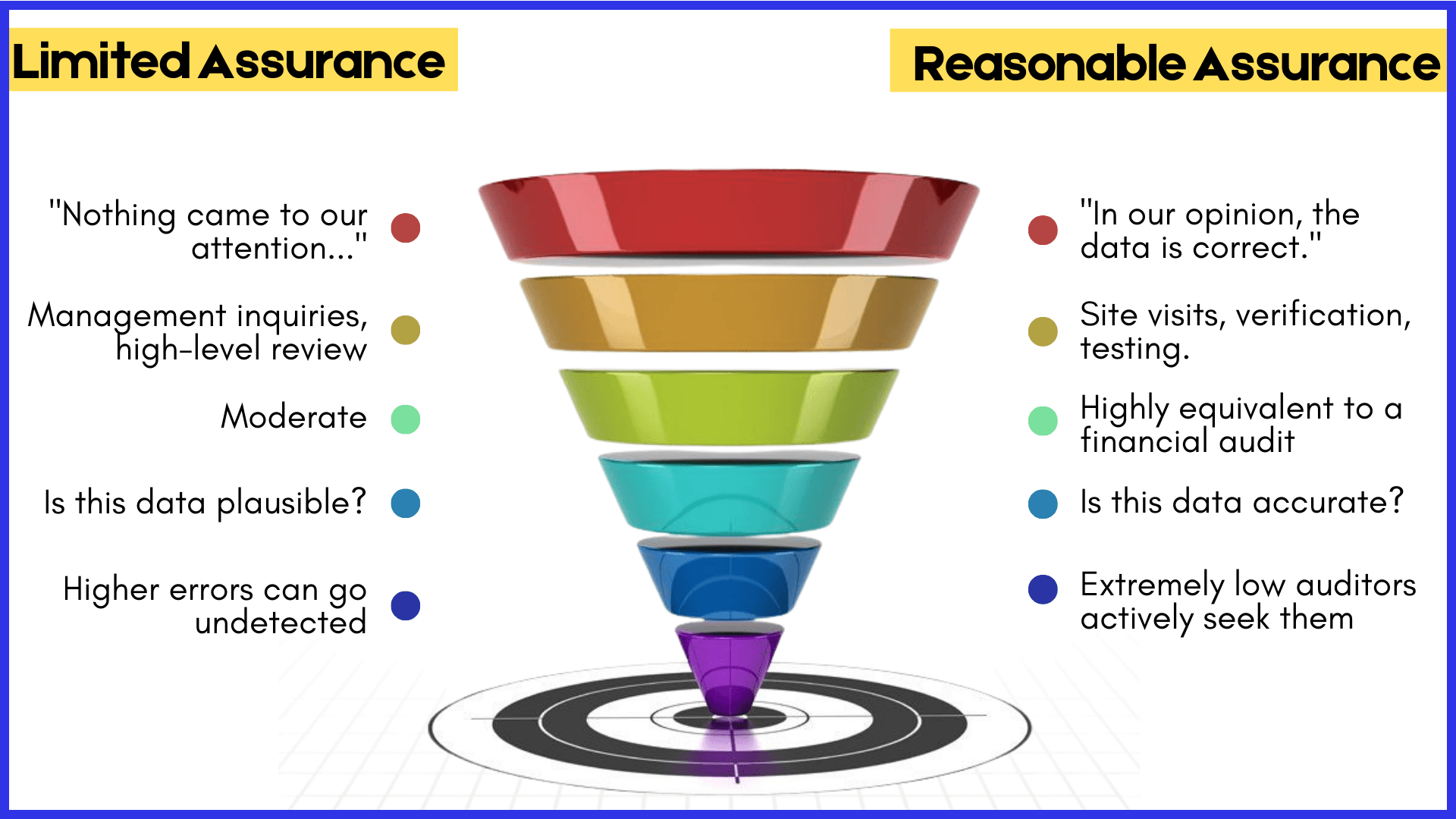

Limited Assurance vs Reasonable Assurance: What Changes for Indian Companies in FY 2026-27

Most companies that have been through an ESG assurance process have experienced Limited Assurance. What's coming in FY 2026-27 is categorically different, and the gap between the two is wider than most compliance teams expect.

| Feature | Limited Assurance | Reasonable Assurance |

|---|---|---|

| The Statement | "Nothing came to our attention..." | "In our opinion, the data is correct." |

| Evidence Required | Management inquiries, high-level review | Site visits, source documents, control testing |

| Confidence Level | Moderate | Highly equivalent to a financial audit |

| Audit Depth | Is this data plausible? | Is this data accurate? |

| Risk of Error | Higher errors can go undetected | Extremely low — auditors actively seek them |

Here is what that difference looks like on the ground.

Under Limited Assurance, an auditor reviews your total electricity bill and moves on. Under Reasonable Assurance, they visit the facility, check individual meter readings, verify that those meters are calibrated, and trace how that data travels from the plant floor to the sustainability report, testing every control point along the way.

If that data journey currently passes through three unlinked Excel sheets managed by different departments, you will not get a clean opinion. You will get a qualified one. And a qualified opinion is not a private conversation with your regulator; it is a disclosed, public signal that your ESG numbers cannot be fully trusted.

The single most important thing to understand about FY 2026-27: Reasonable Assurance doesn't just raise the bar for your auditor. It raises the bar for every internal system, control, and process that feeds your ESG data. That is where the real preparation work lives.

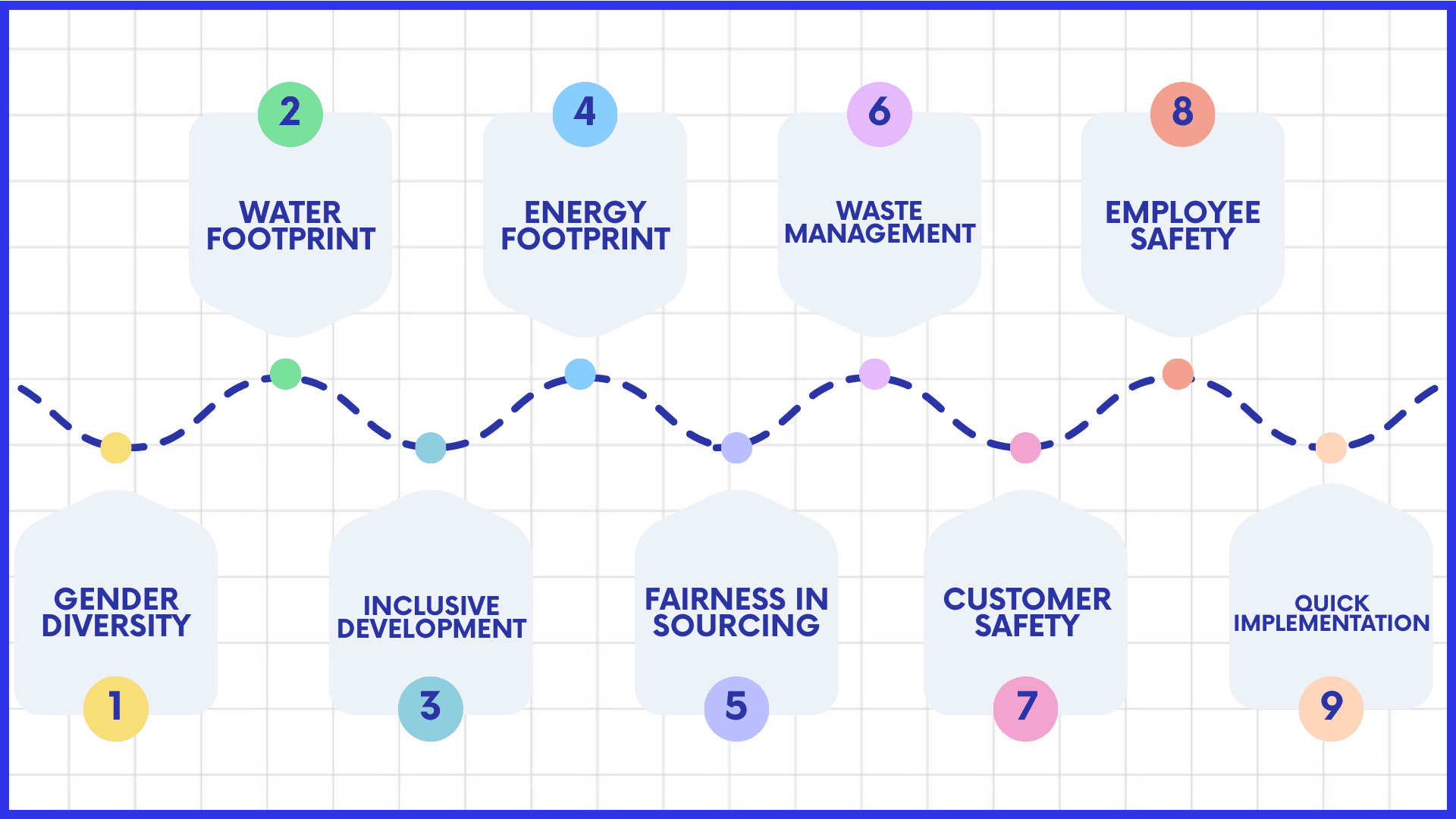

The 9 Mandatory BRSR Core KPIs: What Gets Audited, How, and Where the Boundaries Apply

BRSR Core does not ask companies to report everything. It asks them to report nine things accurately, completely, and to a standard that can withstand forensic scrutiny.

Environmental Metrics:

- GHG Footprint: Gross Scope 1 and Scope 2 emissions in tCO₂e, reported as intensity against PPP-adjusted revenue

- Water Footprint: Total water consumption in kilolitres, with intensity per unit of PPP-adjusted revenue

- Energy Footprint: Total energy consumption in joules or watt-hours, including the share attributable to renewable sources

- Waste Management: Total waste generated, with breakouts for hazardous material and recycling or reuse rates

Social Metrics:

- Employee Safety: Lost Time Injury Frequency Rate (LTIFR) for both employees and contract workers, with underlying man-hours

- Gender Diversity: Female representation at board and senior management levels; gender pay ratio

- Inclusive Development: Net new jobs created in Tier 2, Tier 3, or economically backward districts

- Fairness in Sourcing: Share of procurement by value sourced from MSMEs or small producers

Governance Metric:

Customer Safety: Proportion of products or services attracting safety complaints or data breach incidents

Each attribute carries a defined reporting boundary. The GHG footprint, for instance, must cover all subsidiaries, joint ventures, and leased operational assets, not just the parent company's registered premises. Auditors in FY 2026-27 will examine boundary decisions with particular scrutiny. Selective inclusion is the new form of greenwashing, and it will be caught.

Quick Implementation Tip: Ensure your Denominator (Revenue) is consistent across all intensity ratios. SEBI requires the use of the annual average exchange rate for PPP calculations, as updated by the RBI.

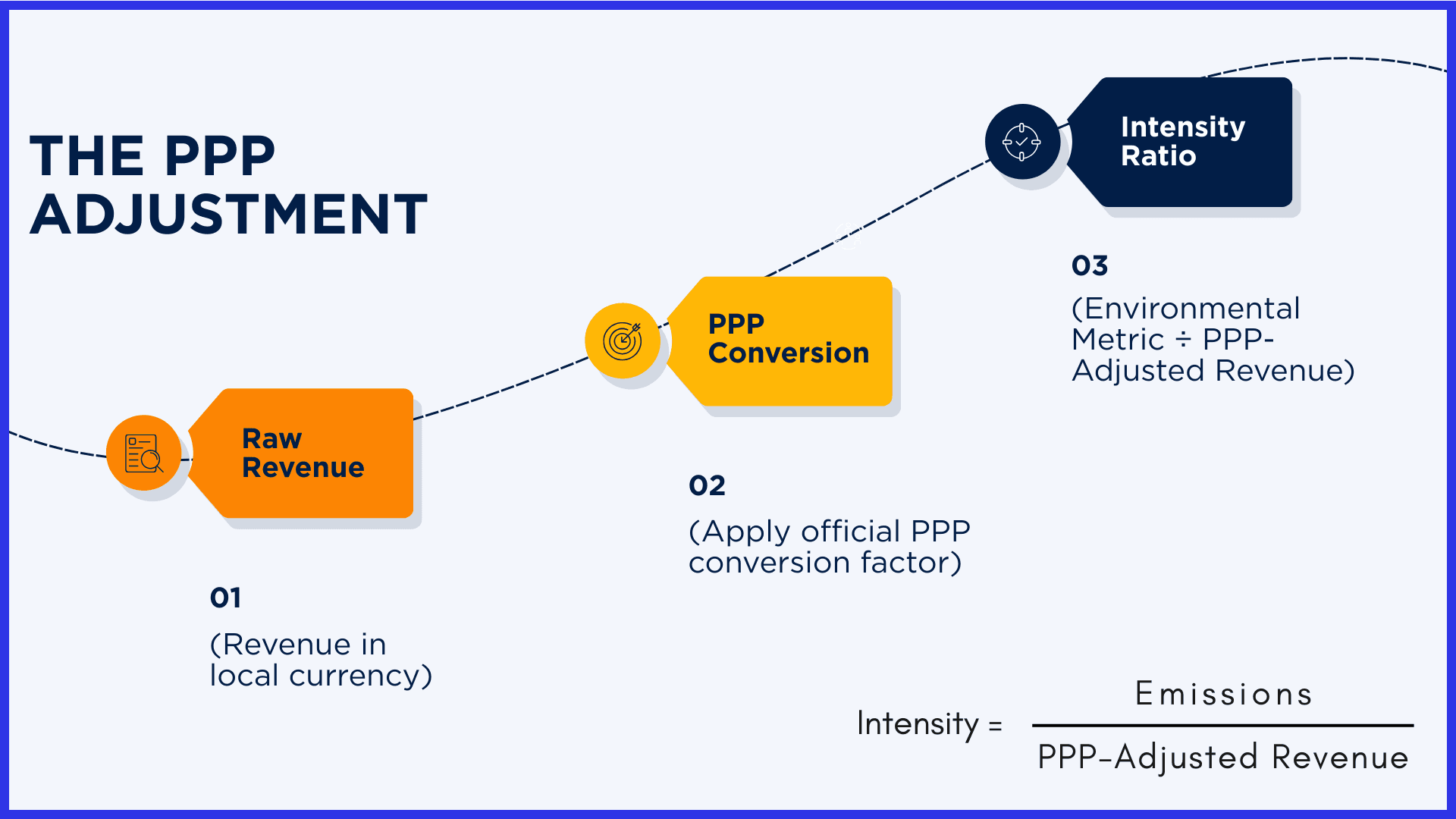

The PPP Adjustment: A Small Formula With Large Implications

One element of BRSR Core that deserves more attention than it typically receives is the Purchasing Power Parity adjustment applied to intensity ratios.

The logic is sound: comparing the carbon intensity of an Indian manufacturer to a European peer using raw revenue creates a distorted picture. A rupee of revenue in India and a euro of revenue in Germany reflect vastly different cost structures and economic contexts.

SEBI's solution is to convert revenue into PPP-adjusted USD before calculating intensity. The formula:

Intensity = Environmental Metric ÷ (Revenue in INR ÷ PPP Conversion Factor)

Using an illustrative PPP factor of ₹23 = $1 USD, a company with ₹10,000 million in revenue and 50,000 tCO₂e in emissions would report an intensity of approximately 115 tCO₂e per million USD a figure directly comparable to global peers.

The RBI publishes updated PPP conversion factors annually. Finance teams must ensure that the denominator used across all nine intensity metrics is consistent, PPP-adjusted, and sourced from the official RBI rate for the reporting period.

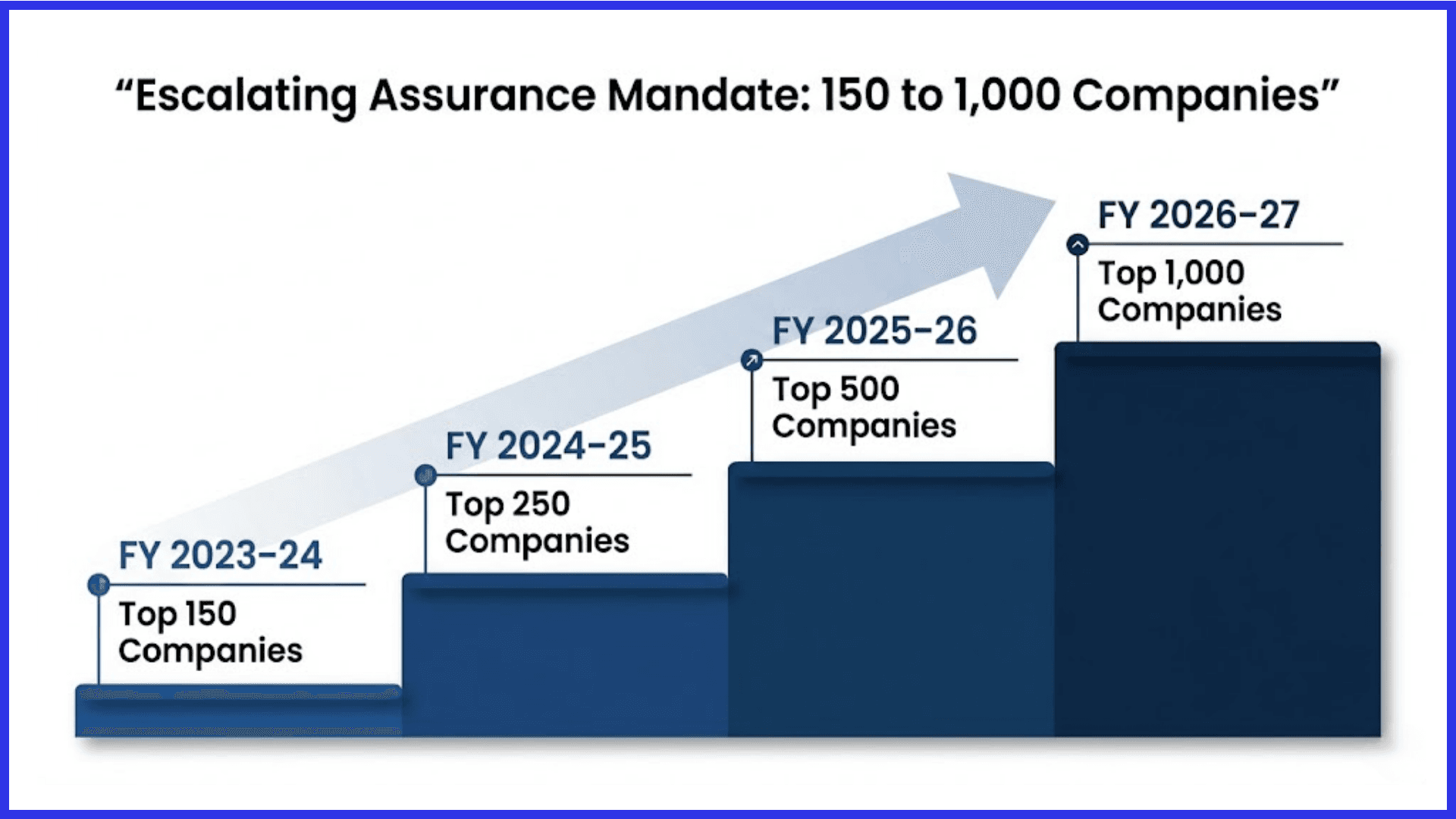

BRSR Core Applicability Timeline: Is Your Company Required to File in FY 2026-27?

SEBI built the BRSR Core rollout as a deliberate staircase, expanding the requirement for Reasonable Assurance one tier at a time.

| Financial Year | Entities Required | Coverage |

|---|---|---|

| FY 2023-24 | Top 150 by market cap | ~150 companies |

| FY 2024-25 | Top 250 by market cap | ~250 companies |

| FY 2025-26 | Top 500 by market cap | ~500 companies |

| FY 2026-27 | Top 1,000 by market cap | ~1,000 companies |

For companies ranked between 500 and 1,000 by market capitalisation, FY 2026-27 is the first year of mandatory Reasonable Assurance. The runway has existed. Companies that chose to wait have now run out of it.

BRSR Core Value Chain Mandate: What India's Top 250 Companies Must Disclose About Their Suppliers

Perhaps the most structurally significant element of BRSR Core and the one most frequently misunderstood is the Value Chain disclosure requirement.

For the Top 250 listed entities specifically, BRSR Core extends beyond the company itself. These companies must collect and disclose the nine Core KPIs for value chain partners that collectively represent at least 75% of their total purchases or sales by value. To make this manageable, SEBI narrowed the obligation to partners who individually account for 2% or more of total procurement or revenue.

Following the March 2025 SEBI circular, value chain disclosures for FY 2025-26 operate on a "comply-or-explain" basis. Mandatory assessment or assurance of value chain data begins in FY 2026-27.

This has a direct implication for unlisted companies: if you supply to a Top 250 entity and your contracts represent 2% or more of their spend, they will ask you for ESG data. Not as a favour. As a compliance requirement. MSMEs and mid-market suppliers that are not yet tracking energy consumption, waste generation, or safety incident rates should begin doing so now, not because they face a SEBI penalty, but because their largest customers soon will.

BRSR Core Implementation Challenges: Solving Data Silos and Value Chain Gaps

The companies that will struggle in FY 2026-27 are not those lacking ambition. They are those who underestimated the operational complexity of Reasonable Assurance.

The first problem is data fragmentation. ESG data in most organisations is spread across engineering logbooks, HR information systems, procurement databases, and utility providers. It has never needed to be consolidated because no one was auditing it. The shift to Reasonable Assurance changes that requirement overnight. The practical solution is ESG data integration, building automated pipelines that pull utility, payroll, and procurement data into a unified system with a preserved audit trail. ERP-connected ESG platforms are increasingly viable, even for companies below enterprise scale.

The second problem is supply chain opacity. Even well-intentioned companies face the reality that many of their key suppliers, particularly MSMEs, lack the infrastructure to report environmental or safety data. The most effective response is supplier enablement: standardised, lightweight data collection templates, webinar-based training, and "report once" portals that reduce the burden on smaller partners. Penalising non-responsive suppliers simply reduces the pool of available supply; enabling them is both more ethical and more practically effective.

The third problem is the talent gap. Sustainability officers who understand environmental science but not audit methodology, and finance professionals who understand audit methodology but not environmental science, are both common. What is rare is someone who speaks both languages fluently. Forward-thinking organisations are creating a dedicated ESG Controller role within the finance function: a person whose job is to apply financial audit rigour to carbon, water, and social data. This role, more than any software platform, is what enables a clean audit opinion.

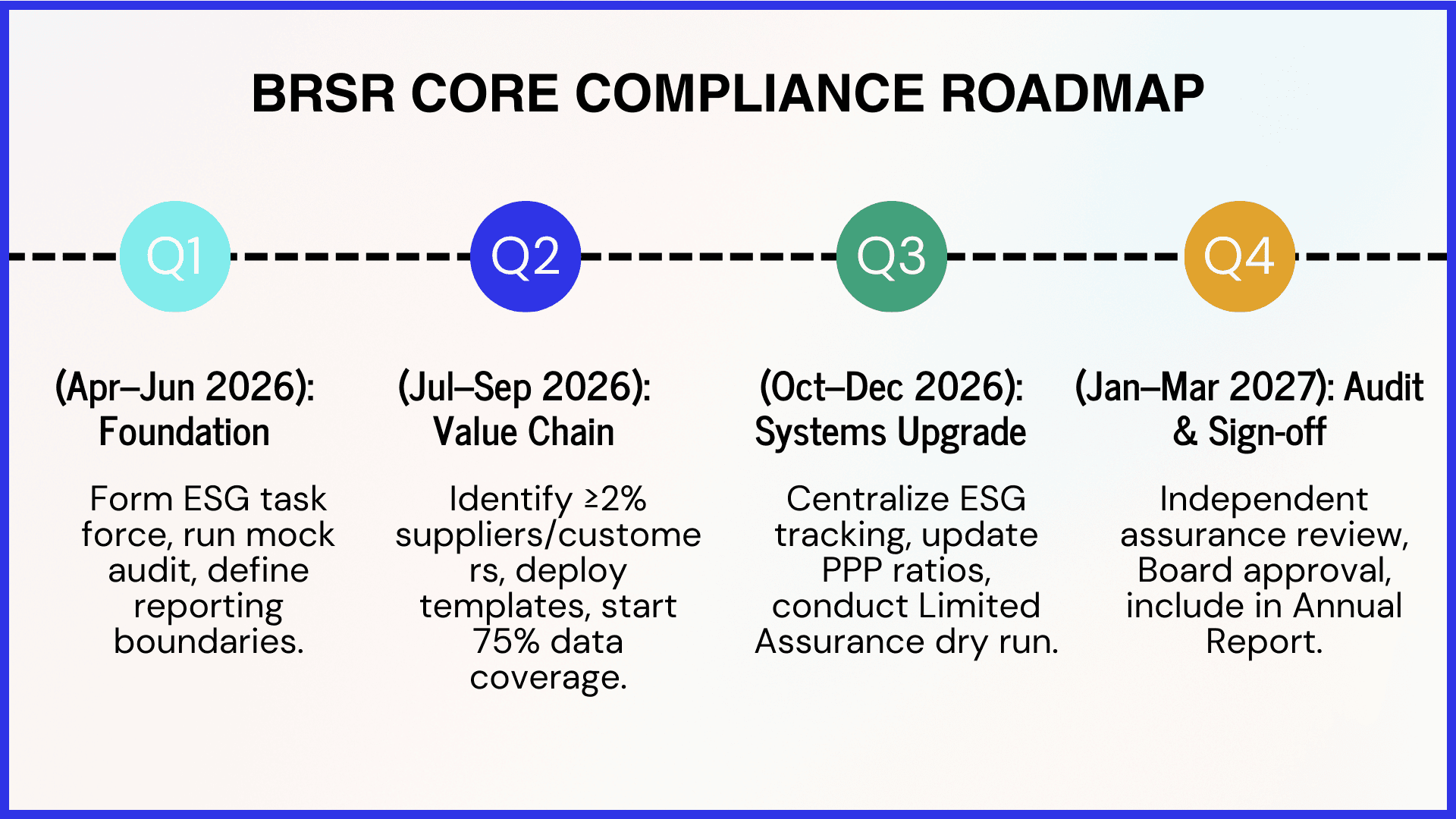

BRSR Core Compliance Roadmap: A Quarter-by-Quarter Action Plan for FY 2026-27

For companies entering the Reasonable Assurance requirement for the first time, the following phased approach reflects what leading companies are already executing.

Q1 (April–June 2026): Establish the foundation. Form a cross-functional ESG task force spanning Finance, Operations, HR, and Procurement. Conduct a mock audit of your current data collection process. Map all subsidiaries and joint ventures that must be included within reporting boundaries.

Q2 (July–September 2026): Engage the value chain. Identify all suppliers and customers individually representing 2% or more of your purchases or sales. Deploy data collection tools or templates. Begin preliminary value chain data collection to meet the 75% coverage threshold.

Q3 (October–December 2026): Harden the systems. Migrate energy, water, and waste tracking to centralised digital platforms. Recalculate all PPP-adjusted intensity ratios using the RBI's updated conversion factors. Commission a preliminary Limited Assurance review as a dress rehearsal before the formal audit.

Q4 (January–March 2027): Execute the audit. The independent assurance provider conducts site visits, source document verification, and internal control testing. The final BRSR Core report is reviewed by the Board ESG Committee and signed off for inclusion in the Annual Report ahead of AGM.

Roadmap Summary: Key Deadlines at a Glance

| Milestone | Deadline | Responsibility |

|---|---|---|

| Data Boundary Finalisation | June 30, 2026 | ESG Task Force |

| 75% Value Chain Mapping | Sept 30, 2026 | Procurement / Supply Chain |

| PPP Intensity Ratios Verified | Dec 31, 2026 | Finance / Sustainability |

| Assurance Opinion Signed | May 2027 (Pre-AGM) | Independent Auditor |

Why This Is Actually Good News for Ambitious Leaders

There is a reasonable temptation to read BRSR Core as a compliance burden another regulatory requirement generating work for finance and sustainability teams with no direct commercial return. That reading is wrong, and the evidence for why it is wrong is now specific enough to be cited.

The most immediate advantage is index eligibility. MSCI ESG Ratings, which govern inclusion in MSCI's ESG indices and inform capital allocation across trillions in AUM, weigh data quality heavily in their methodology. A company with audited, verifiable ESG data is rated more reliably and rated more favourably than a peer with equivalent performance but self-certified disclosure. When Tata Consultancy Services strengthened its ESG data governance and obtained third-party assurance ahead of peers in its sector, the result was a sustained presence in MSCI's ESG Leaders indices. The consequence is not cosmetic: ESG index inclusion affects passive fund allocation, which affects liquidity, which affects the cost of equity capital.

The second advantage is in debt markets. Green bonds and sustainability-linked loans instruments whose pricing is tied to ESG performance require verified data as a structural prerequisite, not a preference. The International Capital Market Association's Green Bond Principles require external review. Lenders' pricing of sustainability-linked facilities requires audited KPI baselines. Companies that cannot provide them are excluded from these instruments or pay more for them. Companies that can provide them access to a financing channel that is both growing and, increasingly, cheaper than conventional alternatives.

The third advantage is internal, and it is the most consistently underappreciated. Companies that build audit-grade ESG data infrastructure almost universally discover operational inefficiencies they had not previously quantified. Not because those inefficiencies were hidden, but because no one had ever been required to measure at that level of granularity. The compressed air system is running above optimal pressure. The utility invoice had been estimated for three years rather than metered. The leased facility that had never been inside the reporting boundary. These are not audit findings. They are cost reduction opportunities surfaced by a process that demanded evidence.

The era in which Indian companies could treat sustainability as a communications exercise is functionally over. What replaces it for those willing to do the work is something more durable: a position built on verifiable fact, legible to investors in London, Singapore, and New York, and capable of supporting financial instruments and index positions that narrative reporting alone cannot unlock.

Conclusion

FY 2026-27 is not a compliance deadline. It is a sorting mechanism.

The companies that treated BRSR Core seriously did not just produce cleaner reports. They found the operational inefficiencies their competitors never measured, earned ESG index positions that self-certified peers cannot access, and opened financing conversations green bonds, sustainability-linked facilities that require verified data as a structural prerequisite. The audit process, in other words, returned more than it cost.

SEBI has created the conditions under which data integrity becomes a competitive asset. A clean Reasonable Assurance opinion signals something no sustainability narrative can replicate: that the numbers behind the story can be trusted. That signal is legible to a fund manager in Singapore the same way it is to one in Mumbai. The organisations that will define Indian corporate leadership over the next decade are not the ones that filed on time. They are the ones who understood what filing required them to build and built it before anyone else made it.

SEBI has made the choice available. The work of making it is yours.

Frequently Asked Questions (FAQs): BRSR & BRSR Core

What is the difference between BRSR and BRSR Core?

The full BRSR is a comprehensive sustainability report covering over 140 indicators across environmental, social, and governance dimensions, self-certified by the company. BRSR Core is a mandatory audited subset of nine specific metrics that require independent Reasonable Assurance, effectively an ESG financial audit. Every Top 1,000 company must submit both; only Core requires external verification.

What does Reasonable Assurance actually mean in practice?

Reasonable Assurance is a positive confirmation, "In our opinion, this data is materially correct" supported by deep evidentiary testing. This includes site visits, calibration checks on measurement equipment, source document tracing, and control environment testing. It is the equivalent of a financial statutory audit applied to ESG data.

What happens if a KPI doesn't apply to our sector?

Companies may report zero and provide a brief materiality explanation under the comply-or-explain framework. Auditors will evaluate whether the non-applicability claim is credible relative to the company's actual operations.

Are there financial penalties for non-compliance?

Yes. Non-filing or materially deficient filing can attract a base penalty of ₹1 crore, ongoing daily fines, and, in serious cases, stock exchange delisting proceedings.

How should we handle value chain partners who won't share data?

SEBI permits the use of reasonable estimates where direct supplier data is unavailable, provided the estimation methodology is clearly disclosed. However, given that assurance becomes mandatory for value chain data in FY 2026-27, companies relying heavily on estimates risk a qualified opinion. Investing in supplier enablement now is more cost-effective than managing a disclosed data gap in an audited report.

If we're an SME supplying to a large listed company, does this affect us?

Directly and increasingly. If you individually represent 2% or more of a Top 250 company's procurement spend, your customer is required to report your ESG data as part of their value chain disclosure. Most will do this by asking you for it. Companies that can provide clean, documented ESG data gain a tangible procurement advantage over those that cannot.