TL;DR: The Business Case for GRI in 2026

In 2026, the Global Reporting Initiative (GRI) transitioned from a voluntary disclosure tool to a critical business intelligence system. It serves as the "interoperability layer" for global ESG compliance, allowing companies to meet multiple regulatory requirements (CSRD, SEC, BRSR) through a single, structured data set.

Key Strategic Takeaways:

- The Three Entry Points: Businesses can report In Accordance with GRI (Full conformance), With Reference to GRI (Specific standards), or use GRI-Referenced disclosures (Specific metrics).

- Double Materiality: Unlike other frameworks, GRI requires you to measure both your impact on the world and the world’s financial impact on your business.

- Commercial ROI: Using structured GRI data replaces "estimated" scores from rating agencies with verified facts, often lowering the cost of capital and winning B2B procurement contracts.

- The 2026 Shift: Success now requires machine-readable data (XBRL), AI-assisted verification, and a focus on transparency regarding data gaps rather than just "polishing" a PDF report.

The Bottom Line: GRI isn't just about transparency; it’s about building a data-driven audit trail that makes your business faster, more fundable, and ready for a regulated global market.

The Report Isn't the Point Anymore

There's a version of sustainability reporting that most companies still practice: a well-designed document, reviewed by legal, approved by leadership, published annually, and largely forgotten.

That version is a liability now.

In 2026, the stakeholders who matter, institutional investors, procurement heads at global enterprises, regulatory bodies across the EU, India, and the US, are not reading your sustainability report. They are running your data through algorithmic scoring systems. They are comparing your disclosures against industry peers. They are penalising gaps, rewarding granularity, and adjusting the cost of your capital accordingly.

The Global Reporting Initiative isn't a reporting framework in any passive sense. It is a structured intelligence system that forces a business to answer the question most companies spend enormous energy avoiding: What does your organisation actually do to the world?

That question is now financially consequential. This guide is for the leaders who understand that.

What Does "Using GRI" Actually Mean? (The 3 Reporting Options)

A business uses GRI by selecting the level of engagement appropriate to its maturity, then structuring its sustainability disclosures according to GRI's framework, at minimum referencing specific standards, at maximum publishing a fully conformant report with a verified GRI Content Index.

This distinction matters far more than most practitioners realise. When a company says it "uses GRI," it could mean one of three formally defined things, and investors, analysts, and procurement teams read the difference precisely.

Option 1: Reporting "In Accordance with GRI Standards"

This is the highest level of GRI engagement. To make this claim, an organisation must apply all requirements of GRI 1 (Foundation), all disclosures in GRI 2 (General Disclosures), all requirements of GRI 3 (Material Topics), and the full management approach and disclosure requirements for each material topic identified.

This level is expected of large enterprises, multinationals, and any company subject to the EU's CSRD or India's BRSR Core assurance requirements. It is what institutional ESG rating agencies like MSCI and Sustainalytics reference when scoring your disclosure quality.

Option 2: "With Reference to GRI"

An organisation using this option applies selected GRI standards to its reporting without claiming full conformance. It must clearly identify which GRI disclosures it has used and how, typically through a partial GRI Content Index.

This is the appropriate starting point for SMEs, first-time reporters, and companies in sectors without a published GRI Sector Standard. It carries genuine credibility with B2B procurement teams and regional investors, without requiring the infrastructure of a full conformant report.

Option 3: "GRI-Referenced" Disclosures

Individual disclosures or data points that follow GRI measurement methodology, for instance, reporting emissions using GRI 305 methodology without producing a comprehensive GRI report. This is common in integrated annual reports, investor presentations, and regulatory filings where companies want to signal methodological rigour on specific metrics.

| Reporting Option | Who It's For | What's Required | Credibility Signal |

|---|---|---|---|

| In Accordance with GRI | Large enterprises, regulated entities | Full GRI 1, 2, 3 + all material topic standards | Highest: ESG ratings, regulatory compliance |

| With Reference to GRI | SMEs, first-time reporters | Selected standards + partial Content Index | Strong: B2B, regional investors |

| GRI-Referenced Disclosures | All sizes | Specific standard methodology applied | Moderate: metric-level credibility |

Understanding which level you are targeting before you begin is not an administrative decision. It determines your data requirements, your resourcing, and the quality of signal you send to the stakeholders who matter most.

What is Double Materiality in GRI Reporting?

Double Materiality in GRI reporting is the principle of assessing both how your business impacts the world (Impact Materiality) and how the external world impacts your financial performance (Financial Materiality).

Most ESG frameworks, like the Sustainability Accounting Standards Board (SASB) or the Task Force on Climate-related Financial Disclosures (TCFD), ask: How does the external world affect your financial performance? GRI asks the inverse first: What does your business do to the world?

Double Materiality requires assessing two distinct dimensions:

-

Impact Materiality (The GRI Lens): Where does your business cause significant positive or negative effects on people, the economy, or the environment? This includes actual and potential impacts on your operations and value chain.

-

Financial Materiality (The ISSB/Investor Lens): Which environmental and social issues are likely to affect your financial performance? GRI’s alignment with frameworks like the EU's Corporate Sustainability Reporting Directive (CSRD) means it now incorporates this dimension too.

The discipline required to answer the impact question honestly, using an auditable methodology, produces institutional self-awareness. The report is the output; the operational insight is the product.

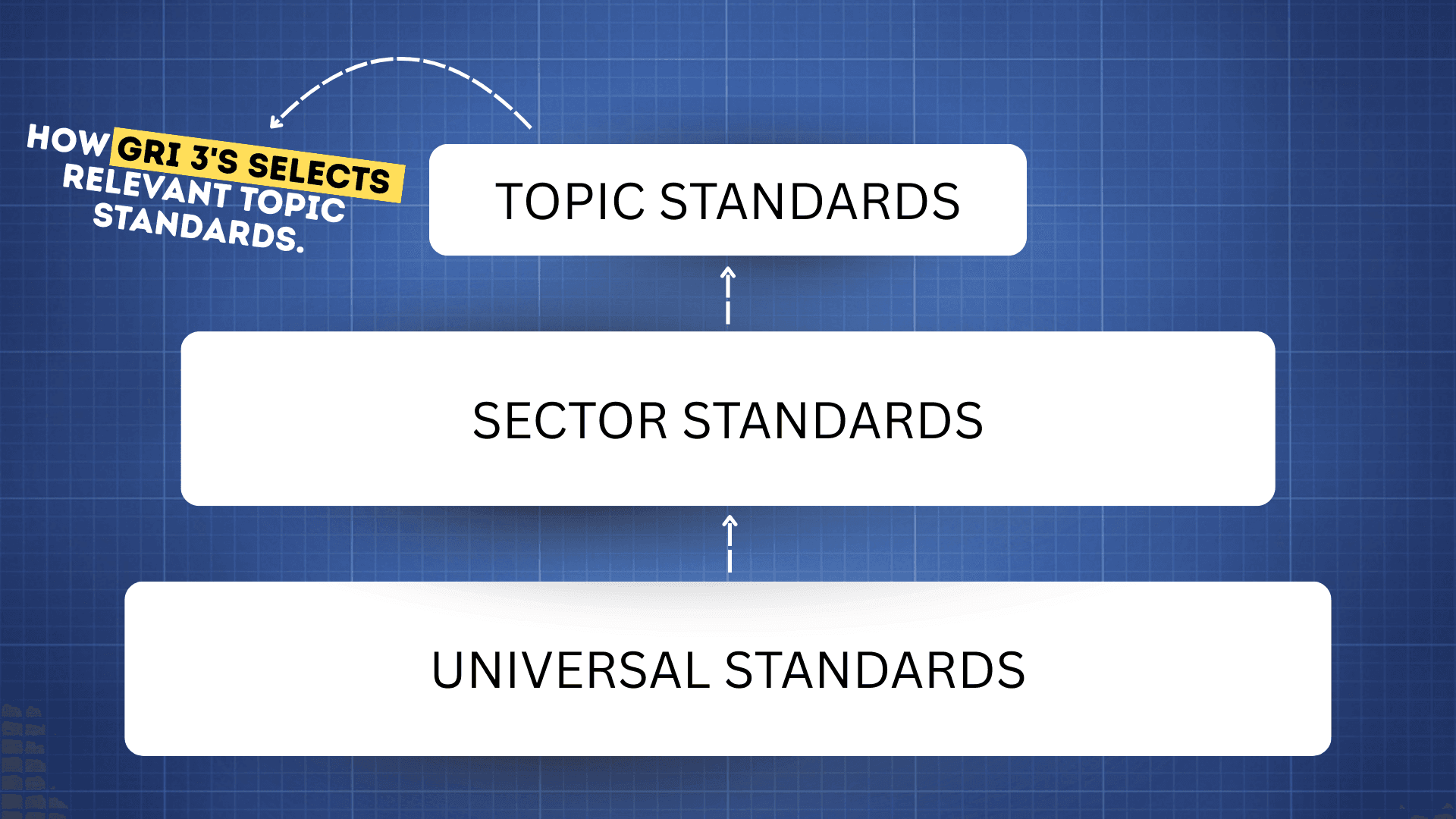

How the GRI Framework is Built

Understanding how GRI actually works matters because the framework is often mischaracterised as either too complex for smaller firms or too generic for meaningful disclosure. It is neither. The system is built in three interconnected layers designed to scale with organisational maturity.

Universal Standards (GRI 1, 2, 3)

These form the structural foundation of every GRI report, regardless of industry or size.

- GRI 1 (Foundation): Establishes the principles of trustworthy reporting (accuracy, verifiability).

- GRI 2 (General Disclosures): Details your governance structure, ownership, and stakeholder engagement.

- GRI 3 (Material Topics): Guides the Materiality Assessment to identify what you will actually report on.

Sector Standards

Impact is not uniform across industries. A financial institution's most significant impacts look nothing like those of a mining company or an agricultural cooperative. GRI's Sector Standards, published for industries including Oil & Gas, Coal, Agriculture, Aquaculture, Financial Services, and more, provide pre-mapped guidance on which topics are likely to be material for specific industries. If your sector has a published standard, it is the most efficient starting point for your materiality process.

Topic Standards

These are where broad ESG commitments become hard data. Organised across economic (GRI 200 series), environmental (GRI 300 series), and social (GRI 400 series) dimensions, each Topic Standard defines exactly what to measure, how to measure it, and what management disclosures are required. GRI 302 for energy consumption. GRI 305 for greenhouse gas emissions. GRI 401 for employment practices. GRI 405 for diversity and equal opportunity.

Together, these three layers do something that most reporting frameworks do not: they generate the kind of structured, machine-readable output that ESG rating agencies, regulatory bodies, and generative AI systems use to evaluate corporate performance.

How to Conduct a GRI Materiality Assessment in 4 Steps

The materiality assessment is the most important step in the entire GRI process. Get it right and everything downstream has clarity and purpose. Treat it as a formality, and you end up producing a report that is technically compliant but strategically useless and experienced analysts can tell the difference.

Here is the GRI-defined four-step process, with the operational detail that most guides leave out.

Step 1: Understand Your Organisational Context

Map your activities, products, services, and value chain relationships. Trace upstream to suppliers and downstream to customers and communities affected by your outputs. Document the sectors you operate in and the geographies you touch. This is the factual foundation; every subsequent decision rests on its accuracy.

Step 2: Identify Actual and Potential Impacts

Using your value chain map, identify where your business causes, contributes to, or is directly linked to significant positive and negative impacts on the economy, environment, or people. This must include Tier 2 and Tier 3 suppliers, not just your direct commercial relationships.

Step 3: Assess Significance

Plot identified topics on a significance scale using two criteria: Severity (assessed by scale, scope, and remediability) and Likelihood. Topics crossing your defined threshold become material topics for reporting.

Step 4: Prioritise and Document

Finalise your material topics and document the entire process in detail, including who you engaged, what evidence informed each decision, and why certain topics were included or excluded. GRI 3 requires this audit trail. It is also what gives your materiality assessment credibility with external assurance providers.

The GRI Content Index: Where Credibility Is Won or Lost

The GRI Content Index is a structured reference table that maps every disclosure in your GRI report to its location in the document. It is a required component of any report claiming conformance with GRI Standards, and it is typically the first place an ESG analyst, rating agency, or procurement team goes when evaluating your report.

What It Must Contain

For each disclosure, the Content Index must specify the GRI Standard and disclosure number, its location in the report, and critically, whether any information has been omitted and why.

That last requirement is widely misunderstood. GRI does not demand perfect data. It demands transparency about the data you have and the data you're still developing. An omission disclosed with a clear explanation and a timeline for resolution signals institutional maturity. A topic that simply doesn't appear signals something else.

The Structure of a GRI Content Index

| GRI Standard | Disclosure | Location in Report | Omission / Reason |

|---|---|---|---|

| GRI 2: General Disclosures | 2-1 Organisational details | Page 4 | — |

| GRI 2: General Disclosures | 2-22 Statement on sustainable development strategy | Page 6 | — |

| GRI 305: Emissions | 305-1 Direct (Scope 1) GHG emissions | Page 34 | — |

| GRI 305: Emissions | 305-3 Other indirect (Scope 3) GHG emissions | — | Data collection in progress; available by the 2027 reporting cycle |

Where to Publish It

The GRI Content Index should be published on your company's website in a dedicated sustainability section, ideally as a standalone HTML page (not just embedded in a PDF), so that ESG analysts using automated tools can access it directly. GRI's XBRL Sustainability Taxonomy makes it possible to publish the Content Index in a machine-readable format, a step that directly improves how rating agencies like MSCI and Sustainalytics ingest your data.

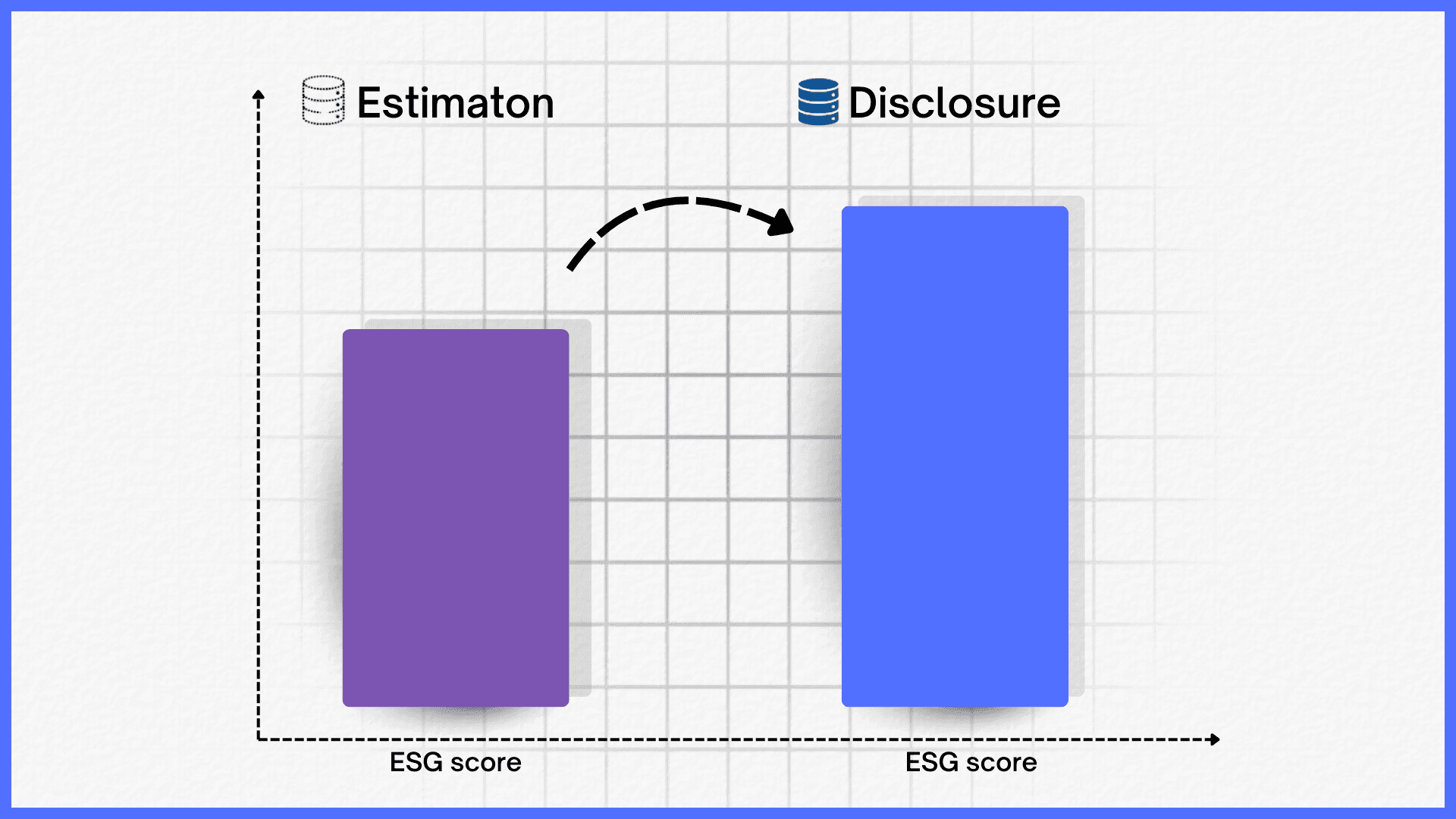

The Commercial Case: How GRI Reporting Improves Your ESG Score

GRI reporting improves your ESG rating by replacing estimated data with disclosed, auditable facts.

Rating agencies like MSCI and Sustainalytics apply an "uncertainty discount" when they have to model your performance using industry proxies. When you disclose energy intensity under GRI 302, employee turnover under GRI 401, or Scope 1 and 2 emissions under GRI 305 in a structured, comparable format, analysts replace their models with your actual figures.

The performance credit you retrieve is real. So are the downstream effects: lower cost of debt through sustainability-linked financing, stronger positioning in B2B procurement processes, and improved standing in ESG-screened institutional portfolios.

The GRI disclosures with the greatest rating impact: GRI 305-1, 305-2, 305-3: Scope 1, 2, and 3 emissions (highest impact) GRI 302-1: Energy consumption (high impact) GRI 401-1 and 403-9: Employee turnover and injury rates (moderate-high impact)

These are not soft indicators. They are the variables that move quantitative ESG scores.

GRI and Global Regulation: One Data Set, Multiple Jurisdictions

For businesses operating across markets, the strategic value of GRI goes beyond reporting quality. It is the interoperability layer that makes multi-jurisdiction compliance economically viable.

| Framework | Scope | GRI Coverage | Remaining Gap |

|---|---|---|---|

| EU CSRD | ~50,000 companies, including non-EU firms with qualifying EU revenue | Approximately 75–80% of ESRS disclosure requirements | Financial materiality formatting; EU-specific audit standards |

| India BRSR | Top 1,000 NSE/BSE-listed companies | The majority of BRSR Core indicators (P3, P5, P6) | Governance items via BSE crosswalk |

| SEC Climate Rules | US public companies | Scope 1/2 emissions; governance disclosures | Precise financial impact quantification |

Companies that build their data infrastructure around GRI are not just satisfying one mandate. They are building the foundation that satisfies all three with targeted supplementary work rather than parallel systems.

Which GRI Topics Matter Most by Sector

The GRI Topic Standards are where intention becomes measurement. Each standard defines precisely what data to collect, how to calculate it, and what context to provide. This is not the place for narrative. It is the place where your ESG commitments are either substantiated or exposed.

| Sector | Core Topic Standards Assessed by Analysts |

|---|---|

| Financial Services | GRI 201 (Economic), 205 (Anti-Corruption), 405 (Diversity), 418 (Privacy) |

| Manufacturing & Tech | GRI 302 (Energy), 305 (Emissions), 306 (Waste), 401 (Employment) |

| Agriculture / F&B | GRI 303 (Water), 305 (Emissions), 308 (Supplier Assessment), 409 (Forced Labour) |

| Mining & Extractives | GRI 302 (Energy), 303 (Water), 305 (Emissions), 411 (Rights of Indigenous Peoples) |

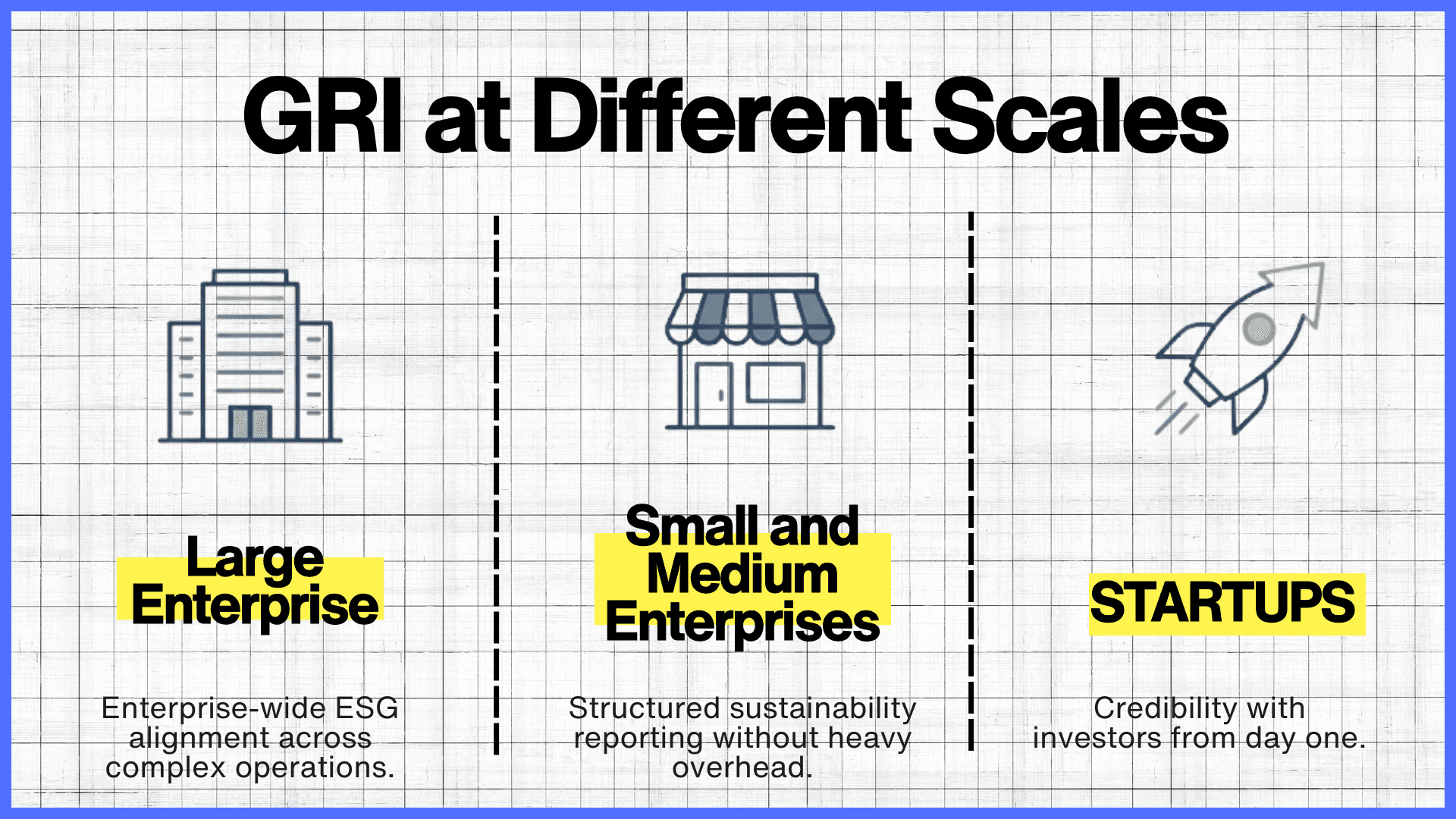

How GRI Works for Your Business Type

One of the most persistent ESG misconceptions is that GRI is only for large enterprises. In 2026, the value of GRI is modular:

Large Corporations: GRI is the infrastructure for sustainability-linked financing. Banks use verified GRI metrics, particularly GRI 302 energy reduction targets, to set and adjust interest rates on sustainability-linked loans. It is also the "reasonable assurance" framework that external auditors reference for annual regulatory filings.

SMEs: Reporting "With Reference to GRI" on five to eight material topics means procurement teams from global enterprises stop sending 40-page supplier questionnaires. Structured GRI disclosures, even partial ones, answer those questions in advance and signal that your business manages risk with professional discipline.

Startups: Venture capital firms increasingly screen early-stage companies for latent ESG risk during due diligence. Adopting core GRI principles before Series A signals institutional readiness. It is a valuation tool.

Five Reporting Mistakes That Undermine Your Credibility

1. Confusing business priority with materiality. GRI materiality is about your impact on the world. What's important internally to leadership is a different and secondary question.

2. Over-reporting. A report covering 30+ topics signals a failure to prioritise. Focused, deeply evidenced disclosure on eight material topics carries far more analytical weight than broad, shallow coverage.

3. PDF-only Content Indexes. Analysts use automated tools. If your Content Index isn't an HTML table accessible to extraction software, it is effectively invisible to the agencies scoring your disclosures.

4. Omitting management approach disclosures. GRI requires you to explain how you manage material topic policies, targets, accountabilities, and resources, not just what the data shows. Numbers without governance context read as performance without commitment.

5. Skipping over data gaps. The "comply or explain" principle is not a weakness; it is a credibility mechanism. Explicitly disclosing what you don't yet measure, with a clear timeline for development, reads entirely differently than a conspicuous silence.

Where GRI Is Heading: 2026 to 2030

Three shifts are already underway and will accelerate.

AI-assisted assurance is becoming standard operating procedure. AI is no longer being piloted for sustainability reporting it is being deployed at scale to scan supply chain datasets, identify anomalies in ESG figures before they reach disclosure, and verify GRI metric calculations against source data in near real time. For companies with complex global operations, AI-assisted audit workflows are becoming the only economically viable path to the data quality that external assurance now requires.

The annual report will be supplemented by real-time data. The GRI report will not disappear; regulatory and investor requirements are too embedded. But it will increasingly sit alongside live performance dashboards that give stakeholders access to material indicators between reporting cycles. The companies building GRI-compatible data infrastructure today are building the foundation for real-time disclosure capability tomorrow.

Multi-framework convergence will reward companies that moved early. The technical alignment between GRI, IFRS Sustainability Standards, and the ESRS is deepening through active cooperation. The expectation among sustainability reporting professionals is that by 2028–2030, a well-constructed GRI dataset will satisfy the substantive disclosure requirements of all three major global frameworks with minimal supplementary work. The companies positioned to benefit are those that built around GRI before the convergence arrived.

Supply chain accountability will extend further than most companies have planned for. The EU Corporate Sustainability Due Diligence Directive (CSDDD) and equivalent national legislation are extending corporate accountability to Tier 2, Tier 3, and beyond. GRI's supplier assessment standards GRI 308, 414, and 412 are directly aligned with these requirements. GRI is becoming due diligence infrastructure, not just a reporting convention.

The Practical Starting Point

The entry cost of GRI is not a 100-page report. It is a decision.

Decide which of the three reporting options fits your current maturity. Conduct a real materiality assessment, not a facilitated internal exercise, but a structured stakeholder-engaged process that identifies where your business has a genuine impact. Build the data infrastructure that makes your disclosures verifiable. Publish your Content Index where analysts can actually find it. Pursue external assurance incrementally.

None of this requires perfection in cycle one. It requires intellectual honesty about what you're measuring and the discipline to improve what you're not. The businesses treating GRI as a compliance obligation will produce compliant reports. The businesses treating it as a strategic intelligence system will produce something more durable: a precise, auditable understanding of what they do, how they operate, and why that distinction matters.

In a market where credibility is a competitive variable, that discipline accrues interest.

Frequently Asked Questions

What is the Global Reporting Initiative (GRI)?

The Global Reporting Initiative is an independent international organisation that provides the world's most widely adopted standards for sustainability reporting. It enables organisations to measure and disclose their environmental, social, and governance (ESG) impacts in a standardised, internationally comparable format. Over 10,000 organisations across more than 100 countries currently report using GRI Standards.

Is GRI reporting mandatory in 2026?

GRI reporting itself remains voluntary. However, it aligns directly with several mandatory regulatory frameworks: the EU's CSRD (aligned with GRI via the ESRS), India's BRSR for the top 1,000 listed companies, and the SEC's climate disclosure rules (aligned with GRI 305 emissions methodology). In practice, a well-constructed GRI dataset typically satisfies 70–80% of mandatory regulatory disclosure requirements as a by-product.

How long does GRI implementation take?

For SMEs producing a focused "With Reference to GRI" report: three to six months. For large enterprises pursuing full conformance: six to twelve months for the initial cycle, with subsequent cycles becoming more efficient as data systems mature. Startups integrating core GRI principles into existing processes can typically produce a reportable output within three to four months.

How much does a GRI report cost?

For SMEs reporting "With Reference to GRI," costs typically range from $15,000 to $30,000, covering consulting, materiality assessment, and design. Large enterprises pursuing full "In Accordance" conformance can expect $100,000 to $250,000 or more, driven primarily by ESG data software implementation and mandatory external assurance fees.

Does GRI reporting satisfy CSRD requirements?

Not entirely, but it provides the substantive majority of what CSRD requires. GRI and EFRAG have achieved high interoperability between GRI Standards and the European Sustainability Reporting Standards (ESRS). A robust GRI dataset covers most of the impact data required. You will still need to format disclosures specifically to ESRS requirements and ensure your financial materiality assessments meet EU audit standards.

Do I need specialist software to publish a GRI Content Index?

Not strictly, but it is strongly recommended in 2026. ESG rating agencies use automated data extraction tools. A Content Index published as a structured HTML page with XBRL digital tagging ensures your data is machine-readable and accurately ingested preventing the "uncertainty discounts" that reduce your ESG score when agencies have to estimate rather than read your figures.