1. What is India's Mandatory CSR Law (Section 135)?

India's Corporate Social Responsibility (CSR) law set a new global standard. With Section 135 of the Companies Act, India actually became the first country anywhere to require companies to spend on CSR legally. This law, which kicked in on April 1, 2014, covers companies that hit any of the following financial benchmarks in the last financial year:

- Net worth ≥ ₹500 crore

- Turnover ≥ ₹1,000 crore

- Net profit ≥ ₹5 crore

Such companies must:

- Form a** CSR Committee** of the Board.

- Dedicate a minimum of 2% of the average net profits from the preceding three years to undertake CSR initiatives.

- Formulate a CSR policy and report the expenditure in the annual report.

CSR activities must be consistent with the provisions of Schedule VII of the Act. These include education, health, equality, the environment, and the development of rural areas.

1.1 The "2% Rule": India’s Unique Global Mandate

India stands alone as the only country in the world that has legally mandated CSR spending. While many other nations encourage corporate philanthropy, India's law is different. It transforms CSR from a simple act of goodwill into a legally enforceable requirement.

CSR in India is not just philanthropy; it is a legal duty. Firms are expected to incorporate socially responsible actions into the governance of the firm as a matter of compliance. Such a legal mandate has generated thousands of crores with a socially responsible purpose every year, thus building a strong pipeline of resources for development activities.

However, this success in capital mobilisation has led to a new challenge: ensuring that spending translates into meaningful, measurable impact. The law has reached a critical inflexion point where output (spending) must evolve into outcome (transformation).

1.2 The Core Problem: Compliance vs. Strategic Impact

How can companies move beyond simply spending 2% to achieve verifiable, equitable, and sustainable social transformation?

The CSR framework? It's great at funding, but awful at fair distribution. Think about it: over 60% of the money is dumped into six states. This accidentally entrenches a compliance-driven, regional focus. Many firms chase quick-win, high-profile projects just to check a box, crowding efforts in cities that are already served. This is why we see:

- Geographic concentration of CSR funds

- Duplication of efforts

- Neglect of the underserved rural and tribal areas

To unlock true impact, companies must shift from checklist-driven compliance to strategic, data-informed interventions. This means:

- Partnering with credible NGOs and local governments

- Using impact metrics and third-party evaluations

- Aligning CSR with national priorities like SDGs and climate resilience

1.3 What This Blog Covers

- The Legal & Philosophical Roots of India's CSR

- The CSR Paradox: Mobilisation vs. Equity Failure

- Who is Leading the Charge? India's Top CSR Spenders

- The Future: From CSR Compliance to ESG Strategy

- Policy recommendations to improve equity and effectiveness

It’s a call to action for companies, policymakers, and civil society to reimagine CSR as a lever for inclusive development rather than just regulatory compliance.

India’s Corporate Social Responsibility legislation has a strong foundation. From ethical capitalism and Gandhian trusteeship to the world’s first legal provisions for CSR under Section 135 of the Companies Act, 2013.

2. The Legal & Philosophical Roots of India's CSR

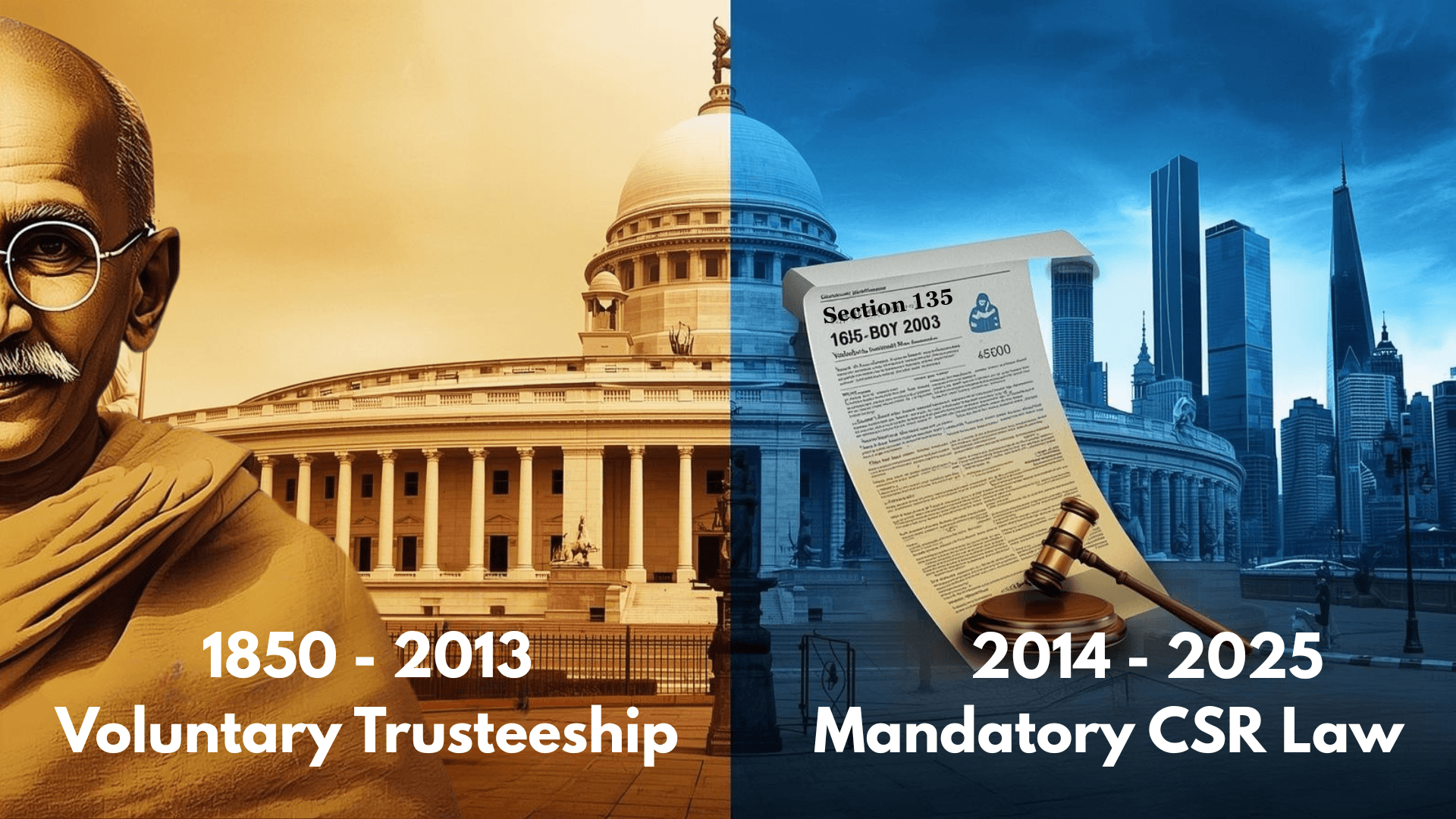

2.1 The History: From Gandhian Trusteeship to Legal Mandate

Pre-Independence Era (1850s–1950s):

In India, corporate social responsibility (CSR) started as voluntary philanthropy, influenced primarily by industrialists such as Jamsetji Tata, Ghanshyam Das Birla, and Lala Shri Ram, who built schools, hospitals, and temples. They exhibited a paternalistic attitude, incorporated by the industrialists, and laid the foundation of industries, along with a sense of moral responsibility for the welfare of workers and the community.

Gandhian Trusteeship:

Mahatma Gandhi`s Theory of Trusteeship became the philosophical cornerstone for CSR in India. Gandhi conceived the idea of the Trusteeship model for the rich. In his view, the rich are simply custodians of their wealth, which ought to be used for the welfare of society. This model of wealth redistribution advocated the idea of moral responsibility without the enforcement of the law. However, Section 135 imposes "Legal Restitution," thus rejecting the "Trusteeship" model.

As India industrialised, CSR remained largely unregulated. However, the growing socio-economic divide and environmental degradation prompted calls for more structured corporate accountability.

The Pivot to Legal Mandate:

2009: The Ministry of Corporate Affairs (MCA) issued Voluntary CSR Guidelines. 2011: The National Voluntary Guidelines on Social, Environmental and Economic Responsibilities of Business (NVGs) were released. 2013: India became the first country to legislate CSR through Section 135 of the Companies Act, 2013, making CSR spending mandatory for qualifying companies.

2.2 What is Section 135? The Legal & Financial Requirements

Applicability: Who Must Comply?

Section 135 encompasses all types of companies operating in India, be they private, public, or foreign, if they satisfied at least one of the following conditions in the previous financial year:

| Financial Threshold | Criteria |

|---|---|

| Net Worth | ₹500 crore or more |

| Turnover | ₹1,000 crore or more |

| Net Profit | ₹5 crore or more |

The Mandate:

Qualifying companies must:

- Form a CSR Committee of the Board.

- Spend at least 2% of the average net profits (as per Section 198) of the past three financial years on CSR activities.

- Disclose CSR policy, projects, and spending in their annual reports and on their websites.

2.3 What is Schedule VII? Where CSR Funds Can Be Spent

Schedule VII of the Companies Act outlines the permissible areas for CSR spending. These include:

- Eradicating hunger, poverty, and malnutrition; promoting healthcare and sanitation.

- Promoting education, including special education and vocational skills.

- Ensuring environmental sustainability, ecological balance, and conservation of natural resources.

- Protection of national heritage, art, and culture.

- Rural development, slum area development, and disaster relief.

- Gender equality, women's empowerment, and support for marginalised communities.

This list is intentionally broad, allowing companies to align CSR with national development priorities like the Sustainable Development Goals (SDGs).

2.4 Accountability & Penalties

The 2019 amendments transformed Section 135 from a 'comply-or-explain' model to a 'comply-or-pay' mandate.

- If companies fail to spend or transfer unspent CSR funds to a specified account, they may face:

- Fines up to ₹1 crore for the company.

- Fines or imprisonment for responsible officers (up to ₹5 lakh or 3 years).

CSR is not just a Board discussion; it is a serious compliance liability.

India’s CSR law is not just a regulatory framework; it’s a moral and strategic instrument to drive inclusive growth. By codifying ethical responsibility into law, it bridges the gap between capital and conscience.

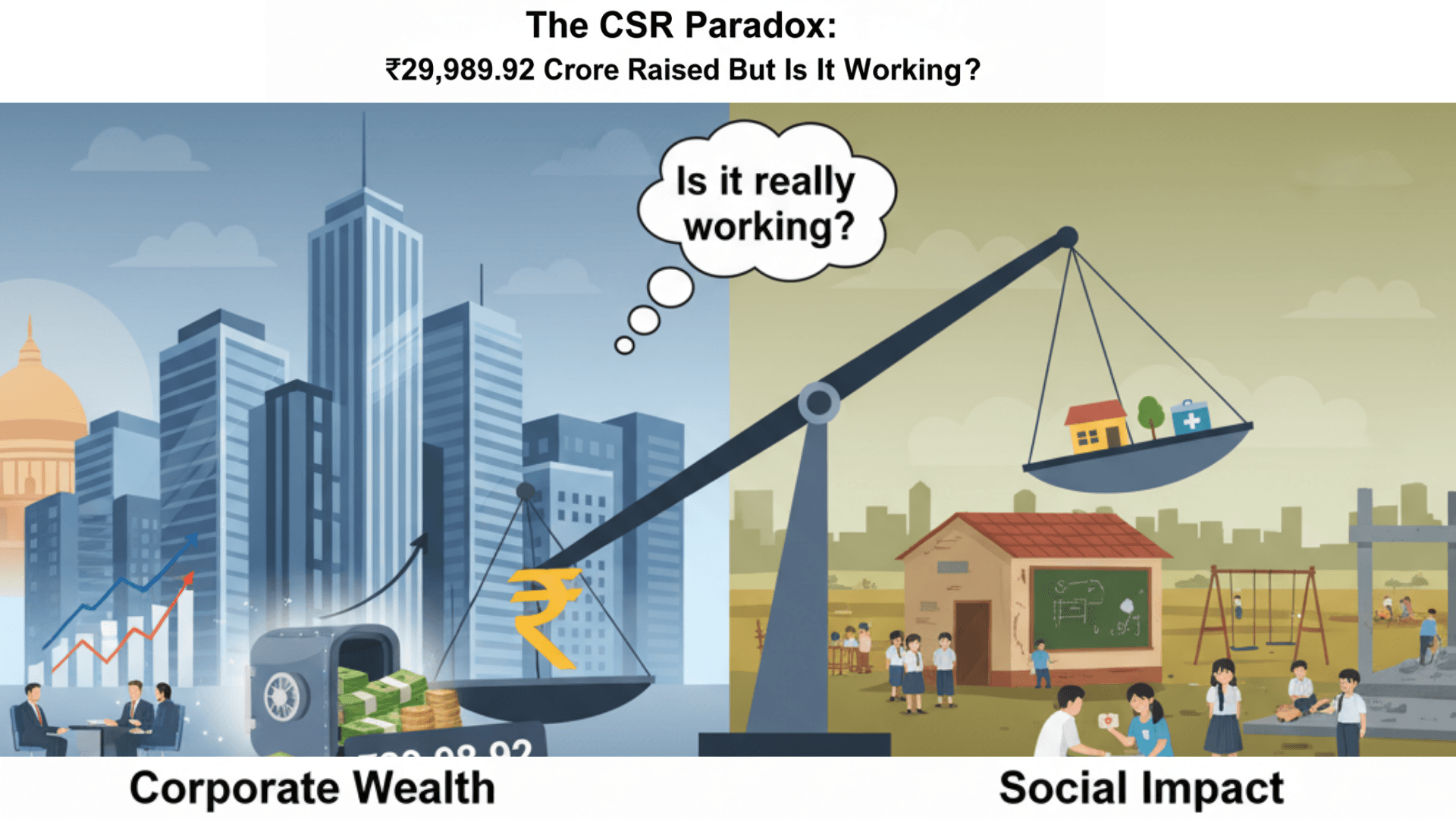

India’s CSR law mobilised ₹29,989.92 crore ($3.6 billion) in 2022–23, but regional and sectoral imbalances reveal a troubling gap between financial output and social impact.

3 The CSR Paradox: ₹29,989.92 Crore Raised, But Is It Working?

India’s mandatory CSR framework has proven its power to mobilise private capital at scale, yet its effectiveness in delivering equitable and strategic impact remains deeply contested.

3.1 Success in Mobilisation (The Output)

In FY 2022–23, Indian companies collectively spent ₹29,989.92 crore on CSR initiatives in India. This figure reflects the strength of Section 135 as a capital mobilisation engine, channelling corporate profits into social development. Leading contributors included:

- Tata Consultancy Services: ₹783 crore

- Tata Steel: ₹481 crore

- Infosys: ₹391.51 crore

This scale of funding rivals national development budgets and has positioned India as a global pioneer in legislated corporate philanthropy.

3.2 The Failure of Equity (The Output Trap)

Geographical Concentration: The Core Flaw

Despite the impressive aggregate spend, 60% of CSR funds are concentrated in just six industrialised states: Maharashtra, Karnataka, Gujarat, Tamil Nadu, Delhi, and Andhra Pradesh. This skew is driven by the “local area preference” clause in the law, which companies interpret as a directive to fund projects near their operational bases.

While this simplifies monitoring and compliance, it inadvertently institutionalises regional inequality. High-need Aspirational Districts, especially in Bihar, Odisha, Jharkhand, and Chhattisgarh receive less than 20% of CSR funds, despite facing acute development deficits.

Sectoral Misalignment

CSR spending also shows sectoral imbalance, with a heavy tilt toward areas already covered by large government schemes:

| Sector | Share of CSR Spend |

|---|---|

| Education | ~37% |

| Healthcare & Sanitation | ~29% |

| Environmental Sustainability | ~9% |

"Environmental Sustainability, the critical 'E' in ESG, receives a disproportionate 9% of funds, indicating a near-term focus on social issues (Education/Health) at the expense of long-term climate resilience.

While education and health are vital, duplicating government efforts without coordination leads to resource inefficiency. Meanwhile, environmental sustainability, critical for long-term national resilience, remains underfunded and underprioritized.

The Compliance Trap

Most companies focus on easily quantifiable outputs the number of school kits distributed, toilets built, or trees planted. These metrics satisfy statutory reporting, but rarely reflect long-term, verifiable change. Few firms invest in:

- Baseline assessments

- Third-party impact evaluations

- Community-led design and feedback loops

This leads to a shallow impact model, where CSR becomes a tick-box exercise rather than a transformative force.

India’s CSR paradox is clear: massive capital, minimal transformation. To unlock its full potential,** companies must shift from compliance-driven spending to outcome-driven strategy** targeting underserved geographies, neglected sectors, and measurable change.

4 Who is Leading the Charge? India's Top CSR Spenders

India’s CSR landscape is shaped by a handful of high-impact corporate leaders who consistently set benchmarks in both financial commitment and strategic execution. These companies go beyond compliance, using CSR as a lever for long-term societal transformation.

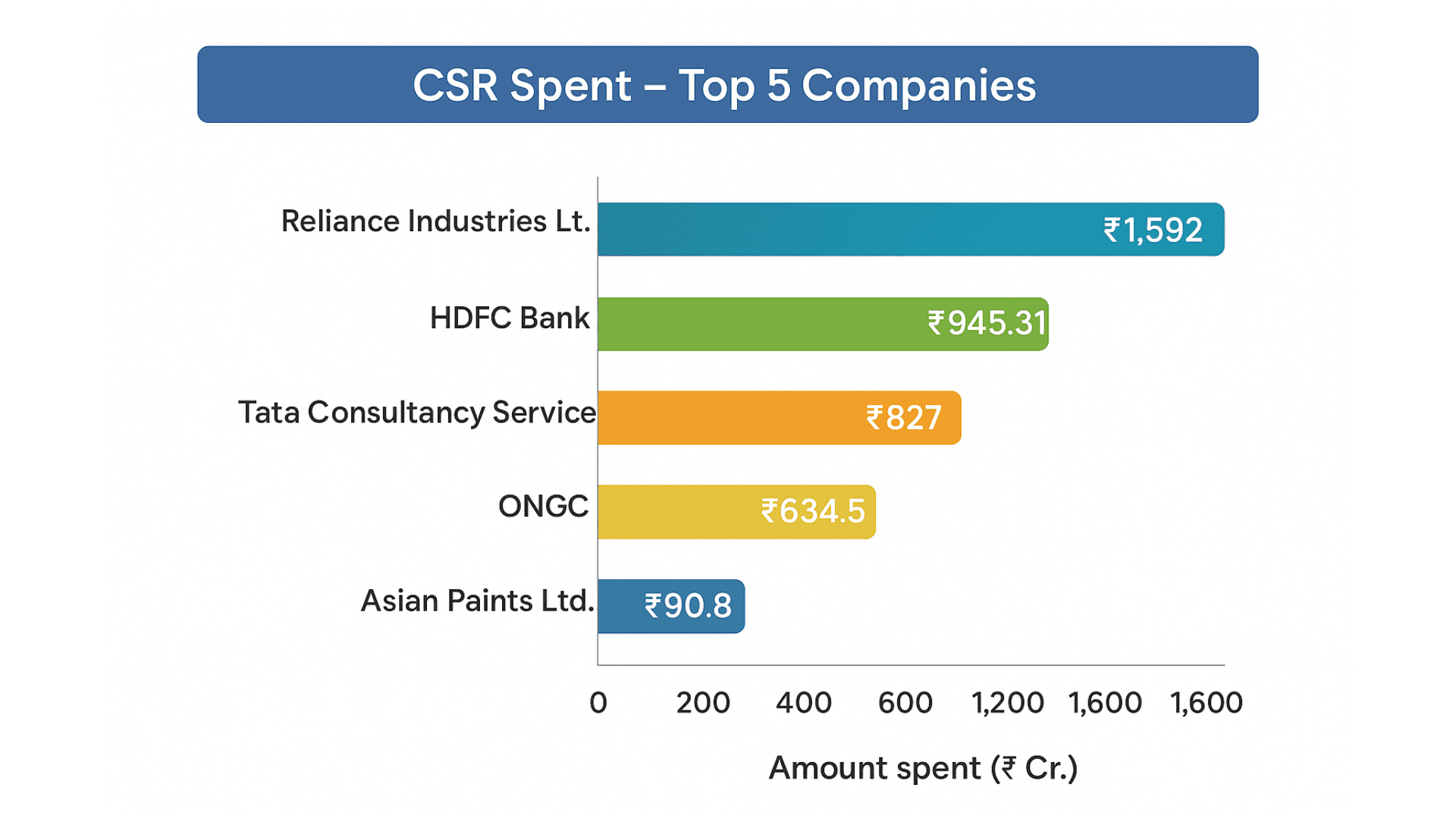

India’s top CSR spenders in FY 2023–24 include Reliance Industries, HDFC Bank, TCS, ONGC, and Asian Paints, each demonstrating scale, focus, and strategic intent in their social investments.

📊 Strategic Spenders and Benchmarks (FY 2023–24)

| Company | CSR Expenditure (₹ Cr.) | Key Focus / Context |

|---|---|---|

| Reliance Industries Ltd. | ₹1,592 | Largest consistent spender; impacted over 76 million lives through health, education, and rural development. (The CSR Journal) |

| HDFC Bank | ₹945.31 | Leading private sector contributor; focuses on financial literacy, education, and skill development. (Fortune India) |

| Tata Consultancy Services | ₹827 | Aligns CSR with tech-driven education, digital literacy, and skilling programs. (Fortune India) |

| ONGC | ₹634.57 | Top PSU contributor; invests in tribal welfare, healthcare, and disaster relief. (Fortune India) |

| Asian Paints Ltd. | ₹90.8 | Focused on vocational training, water stewardship, and community health. (Fortune India) |

These companies collectively represent 17% of India’s total CSR spend, which reached a record ₹34,909 crore in FY24 Fortune India.

4.1 Analysis: What Makes Their CSR Strategy Effective?

Strategic Integration vs. Cheque-Book Philanthropy

Cheque-book philanthropy refers to one-off donations or fragmented projects with limited follow-through. In contrast, strategic CSR involves:

- Long-term platforms: RIL’s CSR is embedded in its business ethos, with multi-year programs in education, healthcare, and rural empowerment.

- Data-driven targeting: TCS and HDFC Bank use analytics to identify gaps and measure outcomes.

- Community ownership: ONGC and Asian Paints engage local stakeholders to co-design interventions.

- Alignment with national goals: These firms often align with SDGs, government schemes, and Aspirational Districts.

Strategic CSR is not just about spending, it’s about sustained impact, scalability, and systemic change.

These leaders show that CSR, when done right, can be a force multiplier for inclusive development. I can now help you build a comparative analysis of their CSR models or visualise this data in a chart, just say the word.

CSR in India is a legal mandate focused on social spending, while ESG is a broader investor-driven framework assessing environmental, social, and governance risks. BRSR bridges the two by standardising disclosures and driving accountability.

5. The Future: From CSR Compliance to ESG Strategy

India’s CSR landscape is evolving rapidly from a compliance-driven mandate to a strategic ESG-aligned framework that attracts investor scrutiny and drives long-term value.

5.1 What is the Difference Between CSR and ESG in India?

| Aspect | CSR | ESG |

|---|---|---|

| Definition | Corporate Social Responsibility: Legally mandated social spending under Section 135 of the Companies Act, 2013 | Environmental, Social, Governance: A global framework used by investors to assess sustainability and risk |

| Nature | Mandatory for qualifying companies | Voluntary but strategic; increasingly demanded by investors and regulators |

| Scope | Focused on social impact (the “S” in ESG) | Covers environmental, social, and governance dimensions |

| Driver | Government regulation | Investor expectations, global benchmarks |

For corporate executives and investors, this pivot is material. CSR reduces the risk of penalty; ESG improves corporate valuation and access to capital. The market now rewards companies whose Section 135 programs strategically feed into their broader, measurable ESG narrative.

India’s CSR law provides the financial and legal foundation for the “S” in ESG, making it a unique blend of statutory obligation and strategic opportunity.

5.2 How Does BRSR Connect to CSR?

BRSR is the Compliance Bridge that forces strategic thinking. By mandating integrated reporting across all nine ESG principles, it ends the era of siloed CSR. Companies must now move from 'What did we spend?' (CSR) to 'What material, verifiable impact did we create?' (BRSR/ESG).

BRSR (Business Responsibility and Sustainability Reporting) is a SEBI-mandated disclosure framework introduced in 2021 for the top 1,000 listed companies. It replaces the older Business Responsibility Report (BRR) and aligns with global ESG standards.

Key Features of BRSR:

- Standardised reporting across nine ESG principles

- Mandatory for listed entities from FY 2022–23

- Covers CSR activities, sustainability risks, and governance practices

The Accountability Link: BRSR forces companies to report CSR and ESG performance transparently, enabling:

Investors to assess sustainability risks Stakeholders to track impact beyond spending Companies to move from “tick-box compliance” to verifiable, strategic impact As EY notes, BRSR simplifies ESG reporting and integrates regulatory frameworks for holistic sustainability governance.

5.3 Top 3 CSR Trends for 2025

1. Digital Tracking

The shift from compliance to ESG mandates a move away from fragmented spreadsheets. Modern CSR is now reliant on technology platforms like Relific.io (or other similar CSR/ESG data management tools) that integrate data from NGO partners, internal departments, and BRSR requirements. This shift enables:

- AI-Powered Reporting: Tools use AI to synthesise scattered data (like impact surveys and expense reports) into auditable, BRSR-ready narratives for the top 1,000 listed companies. This ends the 90% time drain spent on manual data reconciliation.

- Real-time Impact Visualisation: Dashboards provide instant clarity on actual outcomes (e.g., literacy rates improved) rather than just outputs (e.g., books distributed).

2. Climate Focus

With only around 9% of CSR funds aimed at environmental sustainability right now, 2025 will likely see companies:

- Align their projects more closely with climate resilience.

- Companies will finally start building things like cutting pollution, protecting water sources, and funding greener projects right into their main CSR strategies, instead of treating them as an afterthought.

3. Community Co-Creation

CSR is moving from top-down execution to hyperlocal, community-led design. This trend emphasises:

- Participatory planning

- Local ownership

- Long-term sustainability

India’s CSR future lies in strategic ESG integration, where companies are not just spending but transforming. BRSR is the bridge, and 2025 will be the year of measurable, climate-conscious, community-driven impact.

6. Conclusion: A 3-Point Action Plan for Executives

India’s CSR law has achieved what few global frameworks have: mobilising billions in private capital for the public good. With nearly ₹30,000 crore spent annually, it’s a mobilisation success. But this success is shadowed by a growing equity failure; funds are concentrated in already-developed regions, and the impact remains shallow.

The time has come for a strategic pivot. Moving from CSR compliance to ESG integration is no longer a choice; it’s a business imperative. Investors, regulators, and communities are demanding transparency, accountability, and measurable impact.

6.1 3-Point Action Plan for Executives & ESG Investors

A 3-Point Action Plan for Executives & ESG Investors

1. Look Beyond the "Usual 6" States: That old 60/6 CSR concentration model? It's broken. It's time to mandate a change, plain and simple. You need to commit a real, fixed percentage of your budget to India’s Aspirational Districts. This isn't just some 'equity' box-ticking. It’s about getting your impact aligned with the nation's priorities.

2. Make the "E" in ESG About Resilience, Not Just Reporting: That 9% average spend on the environment is a rounding error, not a strategy. True climate action means investing in material resilience. We're talking about integrating water stewardship, the circular economy, and carbon reduction deep into your portfolio. This is how you mitigate real, long-term risk.

3. "BRSR-Proof" Your Metrics to Build Real Trust: Let's be blunt: "vanity outputs" are worthless to serious investors. It's time to abandon them. Invest in credible, third-party impact evaluations and align all your reporting with the BRSR framework. This is the only path to building the credibility that the global investment community actually values.

Faqs

1. What is the difference between CSR, ESG, and BRSR in the Indian context?

This is the most critical strategic question.

-

CSR (Corporate Social Responsibility): This is the legally mandated action and expenditure under Section 135. It is the 2% of profit a company must spend on social projects from the approved Schedule VII list.

-

ESG (Environmental, Social, Governance): This is the holistic framework investors use to measure a company's sustainability, risk, and long-term value. CSR is the primary, mandated driver of the "S" (Social) component in India.

-

BRSR (Business Responsibility and Sustainability Reporting): This is the SEBI-mandated disclosure mechanism. It's the standardized report where a company must publicly state its ESG and CSR performance. BRSR is the "accountability tool" that makes CSR and ESG data transparent to investors.

2. What are the exact thresholds that trigger the 2% CSR law (Section 135)?

The law applies to any company (in the preceding financial year) that meets at least one of these three criteria:

- Net Worth: ₹500 Crore or more

- Turnover: ₹1,000 Crore or more

- Net Profit: ₹5 Crore or more

3. What are the penalties for not spending the 2% CSR amount?

The rules are strict.

- If the amount is for an ongoing project, the unspent funds must be transferred to a special "Unspent CSR Account" within 30 days of the financial year's end and spent within 3 years.

- If the amount is not for an ongoing project, the unspent funds must be transferred to a government-specified fund (like the PM Cares Fund) within 6 months of the financial year's end.

- Failure to do either can result in a penalty of twice the unspent amount (up to ₹1 Crore) on the company and a fine of one-tenth of the unspent amount (up to ₹2 Lakh) on each defaulting officer.

4. Why do most CSR funds go to developed states like Maharashtra and Karnataka?

This is the "geographical imbalance" flaw. It's driven by the "local area preference" clause in the Act.

- The law encourages companies to give preference to the "local area and areas around it where it operates."

- Most companies interpret this as their own operational backyard (factory, corporate HQ) for convenience, monitoring ease, and local PR.

- The problem is that the money tends to stay where the companies are. Most large corporations are based in developed states (think Maharashtra, Karnataka, or Gujarat), so that's where they spend their CSR funds. This means less-industrialized states with high needs, like Bihar, Odisha, and Jharkhand, end up getting overlooked.

5. Can CSR funds be used for environmental sustainability and climate change projects?

Schedule VII of the Companies Act clearly lists "Ensuring environmental sustainability, ecological balance, protection of flora and fauna..." as a key area. But the reality is, this sector only gets about 9% of the money. This isn't the law's fault. It's a strategic gap, where companies are simply choosing to put their funds into more "visible" areas like health and education.

6. How is the 2% CSR spend calculated?

It is 2% of the average net profits of the company made during the three immediately preceding financial years. "Net profit" is calculated as per the company's profit and loss statement (under Section 198 of the Companies Act). Still, it excludes profits from overseas branches and dividends received from other Indian companies that are already CSR-compliant.

7. Is the "local area preference" for CSR spending a strict legal mandate?

No. The law states companies should give "preference" to their local area. It is not a mandatory directive that forbids spending elsewhere. This is a crucial misunderstanding. A company in Mumbai is fully compliant and legally permitted to spend its entire CSR budget in an "Aspirational District" in Odisha. The current imbalance is a result of corporate choice and convenience, not a legal barrier.